Panel debates long-term-rental rule and classification of multifamily buildings under tax bill

May 07, 2026 | Finance, SENATE, Committees, Legislative , Vermont

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

Committee members, legislative counsel and Department of Taxes staff spent a lengthy portion of the hearing hashing through competing approaches to defining "long-term rental" and how to classify multifamily buildings for tax purposes.

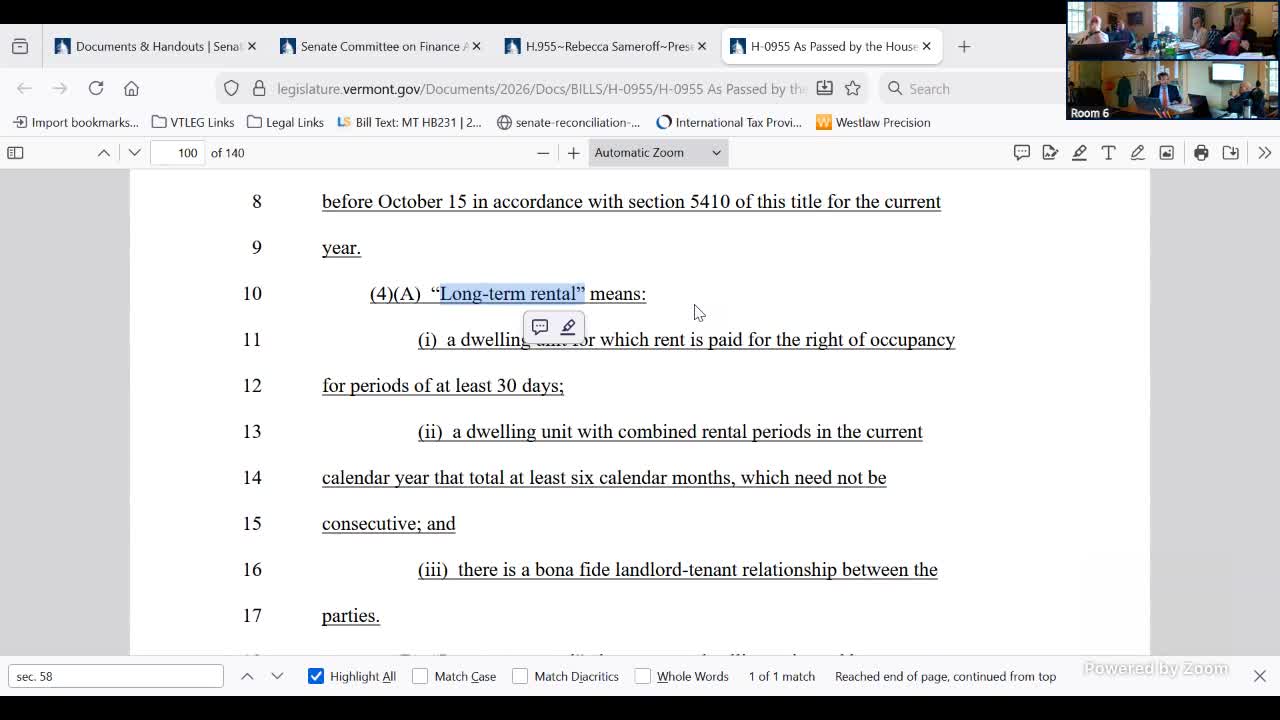

One option discussed mirrored the transfer-tax landlord-certificate approach and used a 30-day threshold (aligned with landlord-tenant law and transfer-tax precedents) plus a bona fide landlord-tenant relationship to identify long-term rentals. Another approach from Ways and Means used a multi-part "and" test that would effectively require a dwelling unit to be rented for six calendar months (not necessarily consecutive) to qualify as a long-term rental.

Kirby Keaton and Rebecca (Deputy Commissioner, Department of Taxes) warned of administrative burdens if landlords of large apartment buildings must fill out a per-unit dwelling-use attestation listing each unit's classification. Tax staff suggested using an existing grand-list category (multifamily/commercial apartment buildings defined as five or more units) to reduce municipal workload, but members and counsel flagged condo ownership and ownership-structure edge cases that complicate a bright-line five-unit rule.

The committee also discussed where to draw the line between regulated lodging establishments (hotels and licensed bed-and-breakfasts) and unregulated short-term rentals; counsel said licensed lodging establishments should be treated as commercial for tax-classification purposes and not as private short-term rentals.

No final statutory text was adopted at this meeting; members asked staff, Tax and housing stakeholders to return with clarifying language, form designs, and examples to avoid creating loopholes or overwhelming municipal systems.

One option discussed mirrored the transfer-tax landlord-certificate approach and used a 30-day threshold (aligned with landlord-tenant law and transfer-tax precedents) plus a bona fide landlord-tenant relationship to identify long-term rentals. Another approach from Ways and Means used a multi-part "and" test that would effectively require a dwelling unit to be rented for six calendar months (not necessarily consecutive) to qualify as a long-term rental.

Kirby Keaton and Rebecca (Deputy Commissioner, Department of Taxes) warned of administrative burdens if landlords of large apartment buildings must fill out a per-unit dwelling-use attestation listing each unit's classification. Tax staff suggested using an existing grand-list category (multifamily/commercial apartment buildings defined as five or more units) to reduce municipal workload, but members and counsel flagged condo ownership and ownership-structure edge cases that complicate a bright-line five-unit rule.

The committee also discussed where to draw the line between regulated lodging establishments (hotels and licensed bed-and-breakfasts) and unregulated short-term rentals; counsel said licensed lodging establishments should be treated as commercial for tax-classification purposes and not as private short-term rentals.

No final statutory text was adopted at this meeting; members asked staff, Tax and housing stakeholders to return with clarifying language, form designs, and examples to avoid creating loopholes or overwhelming municipal systems.

Don't Miss a Word: See the Full Meeting!

Go beyond summaries. Unlock every video, transcript, and key insight with a Founder Membership.

✓

Get instant access to full meeting videos

✓

Search and clip any phrase from complete transcripts

✓

Receive AI-powered summaries & custom alerts

✓

Enjoy lifetime, unrestricted access to government data

30-day money-back guarantee