Committee considers adding equine farming to current-use appraisal with income thresholds

April 25, 2026 | Agriculture, SENATE, Committees, Legislative , Vermont

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

The committee took up a proposal to include equine farming in the state's current-use (use-value) appraisal program by aligning eligibility criteria with the existing framework used for crop-based farming.

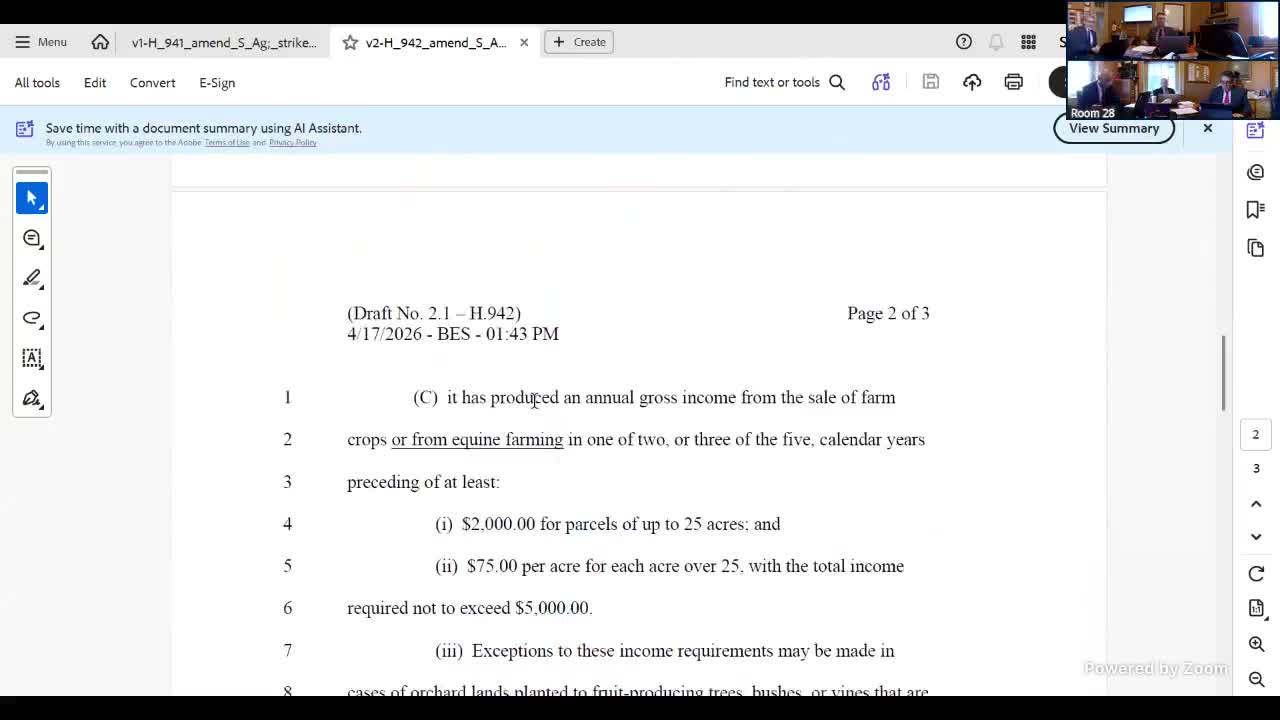

Under the amendment, land used for equine farming could qualify for the program if it produced specified annual gross income from equine activities in a set number of preceding calendar years, with income thresholds scaled to acreage. The draft mirrors the statutory approach for crops and sets a presumption of agricultural use when income criteria are met.

Sponsor Bradley Schoeman said the language follows guidance from the tax department and that the bill would rely on established tax definitions. The amendment would define ‘‘farmer’’ for the equine context using a familiar tax standard: a person who earns at least half their annual gross income from the business of farming as defined in federal tax rules or from equine farming.

The chair noted that the chair of the finance committee appeared receptive to the idea, ‘‘as long as it was bonafide horse farming and not wealthy people looking for a tax break,’’ signaling that the fiscal office will scrutinize eligibility and revenue impacts. A fiscal note was expected soon; sponsors said they would hold final action until that estimate arrives.

Committee members and sponsors said they had conferred with advocates and tax staff to calibrate thresholds and that the department of taxes will be the operational authority for eligibility determinations. No formal vote was taken during the session; sponsors said the committee would await the fiscal note and then return with a motion to move the amendment forward.

If adopted as drafted, the change would make equine operations that meet the income-and-use tests eligible for the same tax appraisal treatment as other agricultural uses, shifting who qualifies for a preferential property tax appraisal but leaving administration to the tax agency.

Under the amendment, land used for equine farming could qualify for the program if it produced specified annual gross income from equine activities in a set number of preceding calendar years, with income thresholds scaled to acreage. The draft mirrors the statutory approach for crops and sets a presumption of agricultural use when income criteria are met.

Sponsor Bradley Schoeman said the language follows guidance from the tax department and that the bill would rely on established tax definitions. The amendment would define ‘‘farmer’’ for the equine context using a familiar tax standard: a person who earns at least half their annual gross income from the business of farming as defined in federal tax rules or from equine farming.

The chair noted that the chair of the finance committee appeared receptive to the idea, ‘‘as long as it was bonafide horse farming and not wealthy people looking for a tax break,’’ signaling that the fiscal office will scrutinize eligibility and revenue impacts. A fiscal note was expected soon; sponsors said they would hold final action until that estimate arrives.

Committee members and sponsors said they had conferred with advocates and tax staff to calibrate thresholds and that the department of taxes will be the operational authority for eligibility determinations. No formal vote was taken during the session; sponsors said the committee would await the fiscal note and then return with a motion to move the amendment forward.

If adopted as drafted, the change would make equine operations that meet the income-and-use tests eligible for the same tax appraisal treatment as other agricultural uses, shifting who qualifies for a preferential property tax appraisal but leaving administration to the tax agency.

Don't Miss a Word: See the Full Meeting!

Go beyond summaries. Unlock every video, transcript, and key insight with a Founder Membership.

✓

Get instant access to full meeting videos

✓

Search and clip any phrase from complete transcripts

✓

Receive AI-powered summaries & custom alerts

✓

Enjoy lifetime, unrestricted access to government data

30-day money-back guarantee