Cullman council approves Rural King development after debate over incentives

April 20, 2026 | Cullman City, Cullman County, Alabama

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

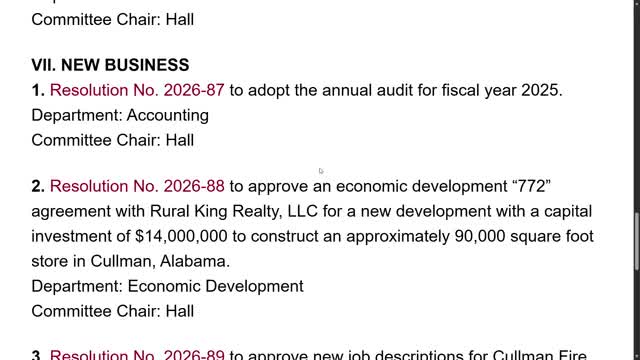

The Cullman City Council on a majority vote approved Resolution 26-88, an economic development agreement with Rural King entities to enable a new $4,000,000, 90,000-square-foot retail store in Cullman.

Council debate centered on whether the city should give direct financial incentives to the retailer or instead invest public funds in infrastructure to support the development and surrounding properties. Councilman Jason Willoughby said he supported retail competition but opposed using tax dollars to give one business an edge over existing local companies. "I'm all for capitalism, but I'm not willing to vote for taking one person's tax dollars and giving them to their competition and creating an unfair advantage," Willoughby said, explaining his opposition and citing other Alabama cities' larger incentive packages as a comparison.

Supporters said the city's package focuses on public infrastructure improvements that will benefit multiple businesses and future developments rather than a sales-tax abatement. Council supporters presented estimated fiscal impacts: officials said the new store is projected to generate about $467,000 in additional funding for local schools in its first year (with $287,000 to Cullman County Schools and $180,000 to Cullman City Schools) and estimated roughly $31,000,000 in total revenue over 20 years. The council and county agreed to a one-time infrastructure contribution rather than a long-term tax abatement.

After discussion and a motion to adopt Resolution 26-88, the measure passed by majority vote. The resolution authorizes the city to enter agreements with Rural King Realty LLC, AJM LLC and Rural King Holdings LLP and to coordinate infrastructure work with Cullman County. The transcript records the outcome as "motion carries"; a detailed roll-call tally was not fully recorded in the public transcript.

The council did not adopt a sales-tax abatement in the motion on the record; council members emphasized the choice of infrastructure investment as an alternative. The agreement as discussed anticipates the developer's capital investment and predicted sales-tax generation; the county and other partners were described as participants in funding infrastructure improvements.

Next steps noted during the meeting included coordination with county officials and further implementation details with the city’s economic development director. The council did not specify a definitive construction start date during the discussion.

Council debate centered on whether the city should give direct financial incentives to the retailer or instead invest public funds in infrastructure to support the development and surrounding properties. Councilman Jason Willoughby said he supported retail competition but opposed using tax dollars to give one business an edge over existing local companies. "I'm all for capitalism, but I'm not willing to vote for taking one person's tax dollars and giving them to their competition and creating an unfair advantage," Willoughby said, explaining his opposition and citing other Alabama cities' larger incentive packages as a comparison.

Supporters said the city's package focuses on public infrastructure improvements that will benefit multiple businesses and future developments rather than a sales-tax abatement. Council supporters presented estimated fiscal impacts: officials said the new store is projected to generate about $467,000 in additional funding for local schools in its first year (with $287,000 to Cullman County Schools and $180,000 to Cullman City Schools) and estimated roughly $31,000,000 in total revenue over 20 years. The council and county agreed to a one-time infrastructure contribution rather than a long-term tax abatement.

After discussion and a motion to adopt Resolution 26-88, the measure passed by majority vote. The resolution authorizes the city to enter agreements with Rural King Realty LLC, AJM LLC and Rural King Holdings LLP and to coordinate infrastructure work with Cullman County. The transcript records the outcome as "motion carries"; a detailed roll-call tally was not fully recorded in the public transcript.

The council did not adopt a sales-tax abatement in the motion on the record; council members emphasized the choice of infrastructure investment as an alternative. The agreement as discussed anticipates the developer's capital investment and predicted sales-tax generation; the county and other partners were described as participants in funding infrastructure improvements.

Next steps noted during the meeting included coordination with county officials and further implementation details with the city’s economic development director. The council did not specify a definitive construction start date during the discussion.

Don't Miss a Word: See the Full Meeting!

Go beyond summaries. Unlock every video, transcript, and key insight with a Founder Membership.

✓

Get instant access to full meeting videos

✓

Search and clip any phrase from complete transcripts

✓

Receive AI-powered summaries & custom alerts

✓

Enjoy lifetime, unrestricted access to government data

30-day money-back guarantee