Jackson workshop frames new budget philosophy and outlines plan tied to a possible 2028 sales-tax measure

March 18, 2026 | Jackson, Teton County, Wyoming

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

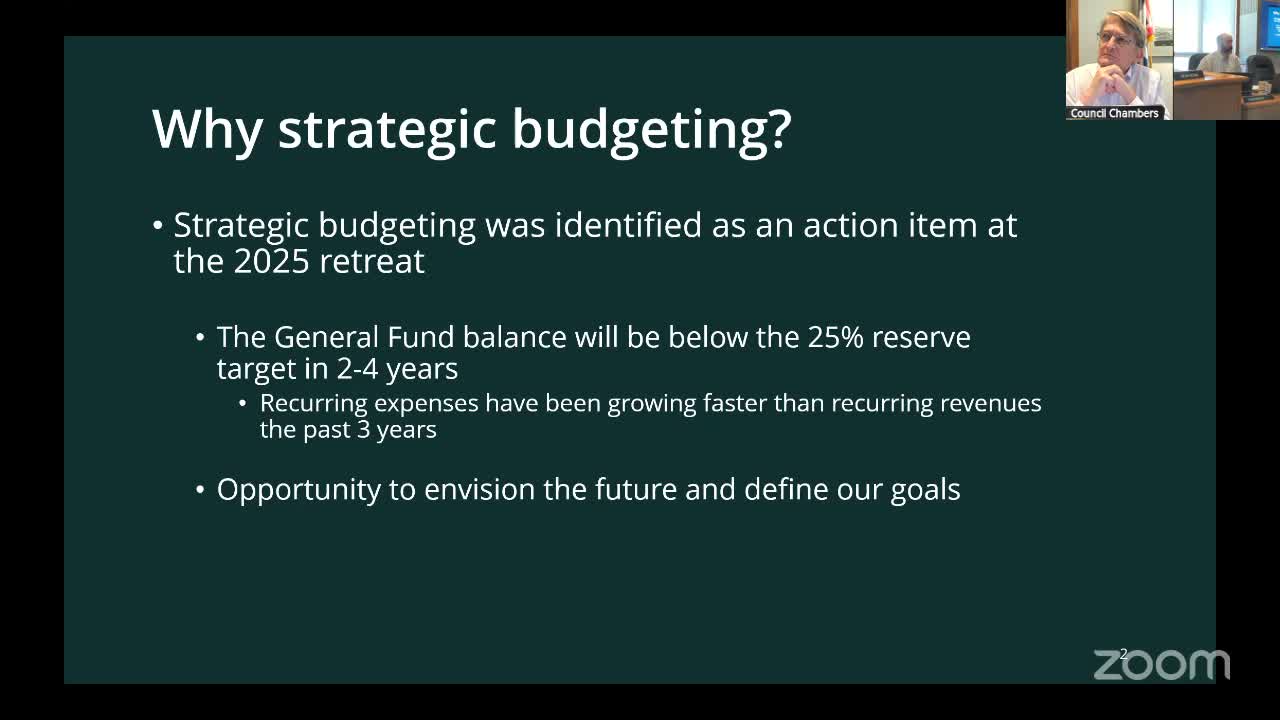

The Jackson Town Manager presented a new strategic budget philosophy at a March 18 special workshop, urging the council to adopt a nonbinding reserve range of 25% to 45% of the general fund and to use an annual target inside that range to guide decisions. "In the next 2 to 4 years, we would be dropping below our 25% reserve target," the Town Manager said, framing the exercise as necessary to avoid a structural deficit.

Why it matters: Staff told the council that recurring expenses have outpaced recurring revenues for several years and that without policy changes the town’s reserves could fall below the proposed 25% floor around 2029–2030. To avoid that outcome, staff recommended limiting new recurring expenses, keeping cost-of-living and merit increases where possible, and adding full-time positions only sparingly.

At the heart of the workshop was a discussion of how the town would act in two scenarios: if a proposed "general penny" sales-tax measure passes in the November 2028 election, and if it does not. The manager described the likely story to tell voters if the measure passes: the town would be able to maintain core services, invest in deferred capital work and fund one-time community priorities such as housing and transportation. "If you added 3 FTEs a year for 10 years, you'd be right back into the deficit where you are today," the Town Manager said, cautioning that one-time revenue is not a long-term fix for recurring costs.

Councilors pressed staff on several specific tradeoffs. One member warned that wording in staff materials — "maximize cost recapture" — could be read as a directive to fully pass service costs to users, which would be a policy choice with distributional consequences. The manager replied that the intention was to capture the general council preference but acknowledged the need for nuance between fees, lodging tax and sales tax. Another councilor asked whether the town had a formal capital reserve target; staff said the capital fund currently holds roughly $9,000,000 but that the town has not yet set a formal policy target for that fund.

On staffing, staff recommended limiting net new FTE growth from the general fund to roughly one position per year for the short-term plan, with exceptions for positions fully offset by new or dedicated revenue. The council debated how to treat vacancies and joint town–county departments; staff said the philosophy is intended to apply broadly but that joint arrangements may require separate treatment given county roles.

Legal and timing questions about the sales-tax measure also came up. The county attorney explained there are statutory mechanics requiring periodic resubmission of certain local tax questions (a typical four-year cycle), and that a mechanism exists to ask voters to make a tax permanent under some statutes. Finance staff said the model used for planning places full revenue impact into FY30 (collections beginning July 2029) for conservative accounting, while noting some receipts could begin affecting FY29 depending on implementation timing.

Staff outlined an outreach plan intended to educate voters and gather feedback before any formal ballot placement. Susan Scarlato, the director of external affairs, described listening sessions with partners (VoicesJH and others) and an online tool (the "Cowboy Family Dashboard") to show residents the approximate value of town services relative to taxes paid. "We're showing people what the expenses are broken into the most simplistic pie chart we can have," Scarlato said, noting staff will compile reports from the outreach and return findings to the council.

What happened procedurally: the only formal vote recorded in the workshop was the approval of the consent calendar (disbursements) at the start of the meeting; the motion passed unanimously. No other ordinances or resolutions were adopted at this session.

Next steps: Staff will translate the workshop feedback into a written budget philosophy and return in May or June with a FY27 implementation plan and more-detailed scenarios for the "general penny" vote. Councilors asked staff to provide clear, voter-focused messaging that emphasizes the choice voters face (maintain current services vs reduce them) and to clarify legal and timing details with county partners before formal ballot decisions.

Why it matters: Staff told the council that recurring expenses have outpaced recurring revenues for several years and that without policy changes the town’s reserves could fall below the proposed 25% floor around 2029–2030. To avoid that outcome, staff recommended limiting new recurring expenses, keeping cost-of-living and merit increases where possible, and adding full-time positions only sparingly.

At the heart of the workshop was a discussion of how the town would act in two scenarios: if a proposed "general penny" sales-tax measure passes in the November 2028 election, and if it does not. The manager described the likely story to tell voters if the measure passes: the town would be able to maintain core services, invest in deferred capital work and fund one-time community priorities such as housing and transportation. "If you added 3 FTEs a year for 10 years, you'd be right back into the deficit where you are today," the Town Manager said, cautioning that one-time revenue is not a long-term fix for recurring costs.

Councilors pressed staff on several specific tradeoffs. One member warned that wording in staff materials — "maximize cost recapture" — could be read as a directive to fully pass service costs to users, which would be a policy choice with distributional consequences. The manager replied that the intention was to capture the general council preference but acknowledged the need for nuance between fees, lodging tax and sales tax. Another councilor asked whether the town had a formal capital reserve target; staff said the capital fund currently holds roughly $9,000,000 but that the town has not yet set a formal policy target for that fund.

On staffing, staff recommended limiting net new FTE growth from the general fund to roughly one position per year for the short-term plan, with exceptions for positions fully offset by new or dedicated revenue. The council debated how to treat vacancies and joint town–county departments; staff said the philosophy is intended to apply broadly but that joint arrangements may require separate treatment given county roles.

Legal and timing questions about the sales-tax measure also came up. The county attorney explained there are statutory mechanics requiring periodic resubmission of certain local tax questions (a typical four-year cycle), and that a mechanism exists to ask voters to make a tax permanent under some statutes. Finance staff said the model used for planning places full revenue impact into FY30 (collections beginning July 2029) for conservative accounting, while noting some receipts could begin affecting FY29 depending on implementation timing.

Staff outlined an outreach plan intended to educate voters and gather feedback before any formal ballot placement. Susan Scarlato, the director of external affairs, described listening sessions with partners (VoicesJH and others) and an online tool (the "Cowboy Family Dashboard") to show residents the approximate value of town services relative to taxes paid. "We're showing people what the expenses are broken into the most simplistic pie chart we can have," Scarlato said, noting staff will compile reports from the outreach and return findings to the council.

What happened procedurally: the only formal vote recorded in the workshop was the approval of the consent calendar (disbursements) at the start of the meeting; the motion passed unanimously. No other ordinances or resolutions were adopted at this session.

Next steps: Staff will translate the workshop feedback into a written budget philosophy and return in May or June with a FY27 implementation plan and more-detailed scenarios for the "general penny" vote. Councilors asked staff to provide clear, voter-focused messaging that emphasizes the choice voters face (maintain current services vs reduce them) and to clarify legal and timing details with county partners before formal ballot decisions.

View the Full Meeting & All Its Details

This article offers just a summary. Unlock complete video, transcripts, and insights as a Founder Member.

✓

Watch full, unedited meeting videos

✓

Search every word spoken in unlimited transcripts

✓

AI summaries & real-time alerts (all government levels)

✓

Permanent access to expanding government content

30-day money-back guarantee