Black Hawk County supervisors weigh using fund balance, tax changes and staff requests in FY27 budget work session

March 03, 2026 | Black Hawk County, Iowa

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

The Black Hawk County Board of Supervisors spent the bulk of its March 3 meeting on the fiscal year 2027 budget, weighing whether to use fund balance to reduce next year’s tax ask and how to fund several personnel and capital priorities.

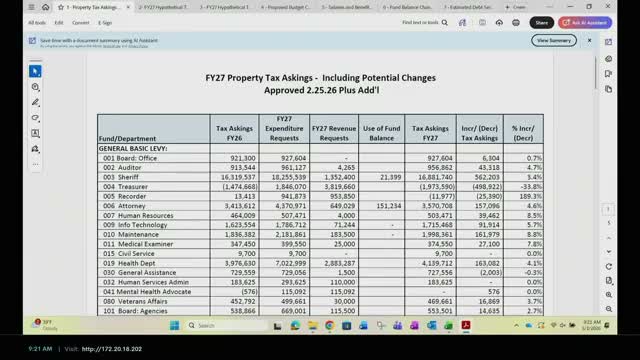

Finance staff summarized a draft budget that, with the adjustments discussed at the meeting, would reduce the immediate shortfall to roughly $4,445. “With the decisions that were made last week, we would end up with only $4,445 left in the hole, so to speak,” Michelle told the board while walking through a spreadsheet of line items and fund balances. Staff presented options including applying $300,000 from the general supplemental fund and $94,885 from rural reserves to smooth next year’s levy rate.

Why it matters: supervisors said the choice to use fund balance now could produce a lower tax base for future years if the state adopts a 2% cap on revenue growth or otherwise changes assessment rules. Staff and supervisors repeatedly cited pending state legislation to change assessor cycles and exemption rules as a major uncertainty that should inform the board’s approach.

Officials said using reserves would modestly lower tax bills for residents this year but could constrain future budgets. The county finance director noted the general supplemental fund held a multi‑million-dollar balance in recent years and that reducing it by $300,000 would still leave the fund in a healthy range.

Board members debated alternatives. Some argued the county should preserve fund balance to avoid constraining future fiscal flexibility. Others favored modest use of reserves now to avoid sharp peaks and valleys in levies, especially if the board proceeds with planned capital projects such as a potential bond for a radio/public-safety system.

The work session also covered equipment and staffing choices. IT staff and supervisors discussed extending replacement cycles for desktop computers from five to six years to capture savings; staff warned that laptops are less tolerant of longer cycles. The board discussed timing for filling a newly budgeted half-time IT position and whether to begin the position mid‑year to test workload needs before committing to a full hire.

On staffing and security, supervisors debated courthouse security models and the number of armed personnel needed if the courthouse continues to limit weapons on premises. That discussion included trade‑offs between hiring deputies and contracting private armed-guard services.

The board scheduled follow-up work sessions to: finalize contract deliverables for proposed partnerships with economic-development groups, refine community-services priorities, and set the public hearing schedule for budget adoption. The county will post the tentative rates and proceed through the statutory hearing process before any final tax levies are adopted.

Finance staff summarized a draft budget that, with the adjustments discussed at the meeting, would reduce the immediate shortfall to roughly $4,445. “With the decisions that were made last week, we would end up with only $4,445 left in the hole, so to speak,” Michelle told the board while walking through a spreadsheet of line items and fund balances. Staff presented options including applying $300,000 from the general supplemental fund and $94,885 from rural reserves to smooth next year’s levy rate.

Why it matters: supervisors said the choice to use fund balance now could produce a lower tax base for future years if the state adopts a 2% cap on revenue growth or otherwise changes assessment rules. Staff and supervisors repeatedly cited pending state legislation to change assessor cycles and exemption rules as a major uncertainty that should inform the board’s approach.

Officials said using reserves would modestly lower tax bills for residents this year but could constrain future budgets. The county finance director noted the general supplemental fund held a multi‑million-dollar balance in recent years and that reducing it by $300,000 would still leave the fund in a healthy range.

Board members debated alternatives. Some argued the county should preserve fund balance to avoid constraining future fiscal flexibility. Others favored modest use of reserves now to avoid sharp peaks and valleys in levies, especially if the board proceeds with planned capital projects such as a potential bond for a radio/public-safety system.

The work session also covered equipment and staffing choices. IT staff and supervisors discussed extending replacement cycles for desktop computers from five to six years to capture savings; staff warned that laptops are less tolerant of longer cycles. The board discussed timing for filling a newly budgeted half-time IT position and whether to begin the position mid‑year to test workload needs before committing to a full hire.

On staffing and security, supervisors debated courthouse security models and the number of armed personnel needed if the courthouse continues to limit weapons on premises. That discussion included trade‑offs between hiring deputies and contracting private armed-guard services.

The board scheduled follow-up work sessions to: finalize contract deliverables for proposed partnerships with economic-development groups, refine community-services priorities, and set the public hearing schedule for budget adoption. The county will post the tentative rates and proceed through the statutory hearing process before any final tax levies are adopted.

View the Full Meeting & All Its Details

This article offers just a summary. Unlock complete video, transcripts, and insights as a Founder Member.

✓

Watch full, unedited meeting videos

✓

Search every word spoken in unlimited transcripts

✓

AI summaries & real-time alerts (all government levels)

✓

Permanent access to expanding government content

30-day money-back guarantee