LBO: heating-fuel, water and sewer sales-tax exemptions amount to roughly $344 million in FY2026; members press for distributional detail

February 26, 2026 | 2026 Legislature MN, Minnesota

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

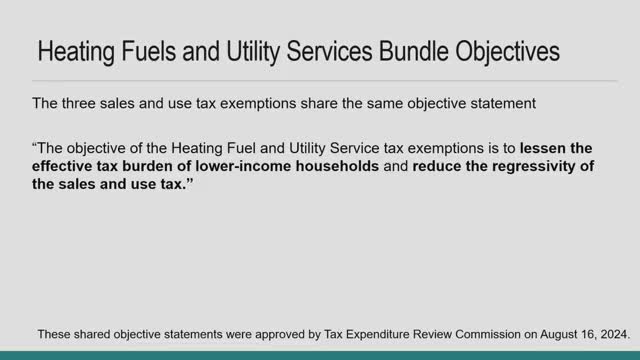

LBO presented an evaluation of three sales-and-use-tax exemptions intended to reduce tax burdens for low-income households: residential heating fuels (enacted 1978 and expanded in 1984), residential water services (enacted 1979), and sewer services. The Department of Revenue’s fiscal estimate cited in the presentation put foregone revenue at about $344,000,000 for fiscal year 2026.

Vlad Flouimo (LBO) said the evaluation relies on the Department of Revenue’s incidence work and county/utility data where available. LBO staff reported that the exemptions reduce the regressivity of the sales-and-use tax and estimated average annual savings by income decile (for example, households making less than $25,000 save on average about $68, while households with much higher incomes save more in absolute dollars), but stressed that the data used are subject to limitations and simulations.

Representative Lee and Representative Wiener asked for more detail on how those averages were derived, whether household-size and metro-versus-outstate breakdowns were available, and whether a 7-county metro comparison had been done; LBO said a regional breakdown specific to Xcel Energy median utilization was provided as follow-up and that the office would furnish further data.

LBO staff and committee members discussed policy alternatives and tradeoffs: one member asked whether $344 million a year might be a less-targeted way to spend those resources compared with direct assistance programs focused on heating needs. LBO noted limitations in isolating policy effects and in some cases limited historical data for older exemptions enacted decades ago.

Next steps: committee members requested regional and demographic incidence breakdowns; LBO agreed to provide the data requested for committee review.

Vlad Flouimo (LBO) said the evaluation relies on the Department of Revenue’s incidence work and county/utility data where available. LBO staff reported that the exemptions reduce the regressivity of the sales-and-use tax and estimated average annual savings by income decile (for example, households making less than $25,000 save on average about $68, while households with much higher incomes save more in absolute dollars), but stressed that the data used are subject to limitations and simulations.

Representative Lee and Representative Wiener asked for more detail on how those averages were derived, whether household-size and metro-versus-outstate breakdowns were available, and whether a 7-county metro comparison had been done; LBO said a regional breakdown specific to Xcel Energy median utilization was provided as follow-up and that the office would furnish further data.

LBO staff and committee members discussed policy alternatives and tradeoffs: one member asked whether $344 million a year might be a less-targeted way to spend those resources compared with direct assistance programs focused on heating needs. LBO noted limitations in isolating policy effects and in some cases limited historical data for older exemptions enacted decades ago.

Next steps: committee members requested regional and demographic incidence breakdowns; LBO agreed to provide the data requested for committee review.

Don't Miss a Word: See the Full Meeting!

Go beyond summaries. Unlock every video, transcript, and key insight with a Founder Membership.

✓

Get instant access to full meeting videos

✓

Search and clip any phrase from complete transcripts

✓

Receive AI-powered summaries & custom alerts

✓

Enjoy lifetime, unrestricted access to government data

30-day money-back guarantee