Attorney General staff warn elders face rising losses as banks, crypto and social media fuel scams

February 20, 2026 | Legislative Sessions, Washington

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

Attorney General consumer protection staff told a legislative committee on Feb. 20 that older adults are increasingly targeted by imposter and investment scams and typically lose larger amounts when victimized.

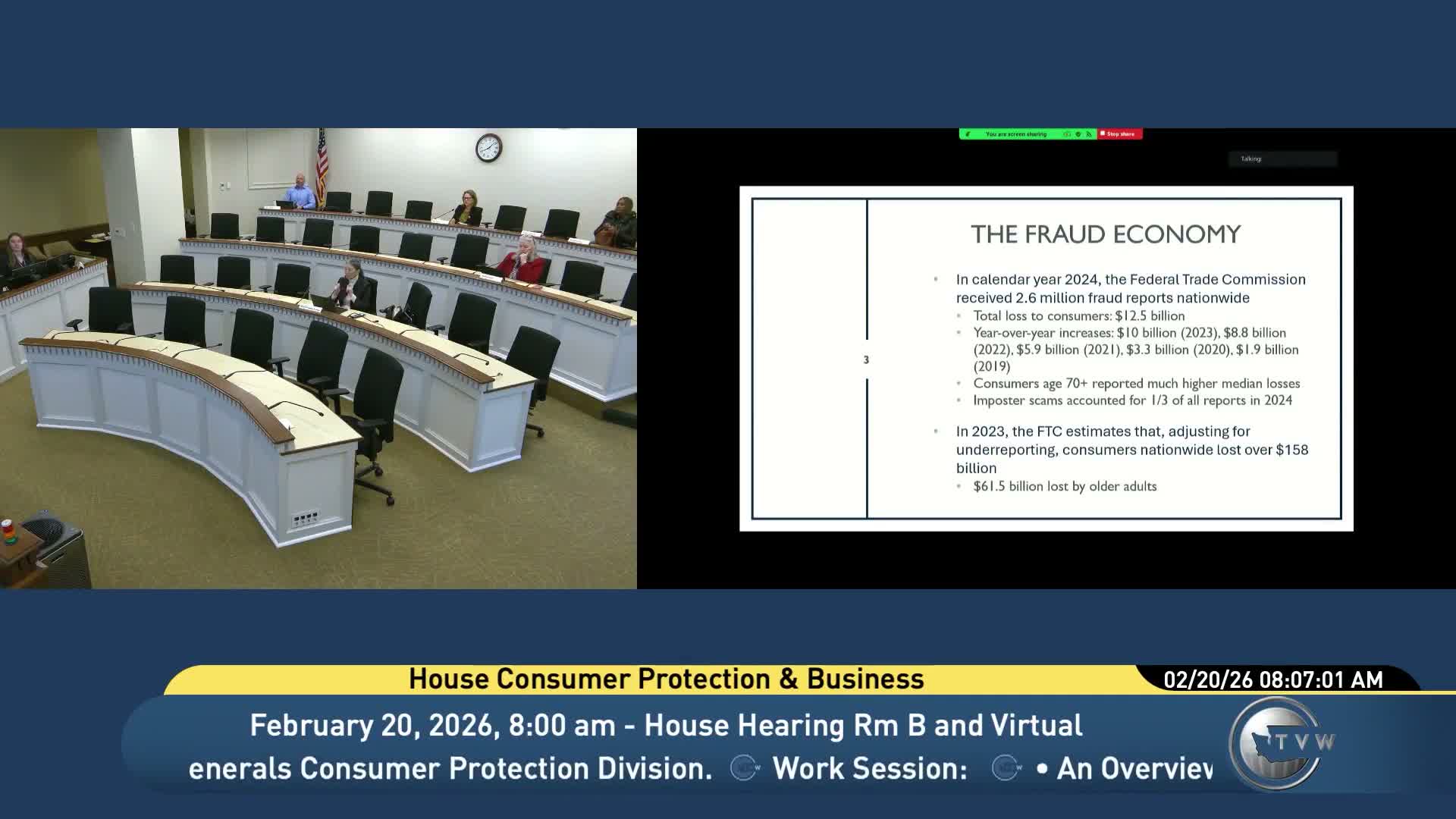

Sean Colgan, an assistant attorney general in the Consumer Protection Division, presented FTC 2024 data showing the agency received about 2,600,000 fraud reports last year with $12.5 billion in reported losses nationwide; Washington’s share was cited as $297,750,000. Colgan said older adults — especially people 70 and up — report much higher median losses even if the number of incidents is similar across age groups.

Why it matters: Colgan said the combination of outreach channels and faster, irreversible payment methods is increasing the harm. "In the case of bank transfers, once it hits the receiving account, scammers just empty that account or close it. It's gone," he said, stressing that bank wires and cryptocurrency transactions are particularly difficult to reverse.

Colgan outlined patterns seen in FTC and state data: imposter scams account for about one‑third of reports, social media‑originated schemes account for a disproportionately large share of dollars lost, and investment scams — though fewer in number — cause especially large losses per incident. He noted that credit and debit cards top by count of transactions, but bank transfers and crypto account for larger shares of total dollar losses.

What the office can and can’t do: Colgan described the AGO's consumer resource center and a dispute resolution program that can recover funds when the merchant or business is legitimate. But he emphasized limits: "These attacks often come from overseas, and they're mounted in a way that makes them virtually untraceable," he said, adding that by the time many complaints arrive, the funds are gone or the perpetrators are outside the AGO's jurisdiction.

Policy options and prevention: The AGO recommended focusing legislative attention on back‑end payment safeguards that slow or limit irreversible transfers (waiting periods, transaction limits or clearer warnings). Colgan said consumer education remains a priority and urged people to report suspected scams to the Attorney General’s consumer resource center and to other agencies such as the Department of Financial Institutions.

The committee exchanged questions with AGO staff about underreporting, definitions of "older adult" (the FTC generally uses 60+ but losses spike at 70+), and whether state‑level action can affect federally chartered banks. Colgan said state options are limited for federally chartered institutions but recommended exploring state action on cryptocurrency kiosks and other points of vulnerability.

What’s next: The presentation prompted interest from members about legislative and regulatory responses; no formal action or vote was taken at the work session.

Sean Colgan, an assistant attorney general in the Consumer Protection Division, presented FTC 2024 data showing the agency received about 2,600,000 fraud reports last year with $12.5 billion in reported losses nationwide; Washington’s share was cited as $297,750,000. Colgan said older adults — especially people 70 and up — report much higher median losses even if the number of incidents is similar across age groups.

Why it matters: Colgan said the combination of outreach channels and faster, irreversible payment methods is increasing the harm. "In the case of bank transfers, once it hits the receiving account, scammers just empty that account or close it. It's gone," he said, stressing that bank wires and cryptocurrency transactions are particularly difficult to reverse.

Colgan outlined patterns seen in FTC and state data: imposter scams account for about one‑third of reports, social media‑originated schemes account for a disproportionately large share of dollars lost, and investment scams — though fewer in number — cause especially large losses per incident. He noted that credit and debit cards top by count of transactions, but bank transfers and crypto account for larger shares of total dollar losses.

What the office can and can’t do: Colgan described the AGO's consumer resource center and a dispute resolution program that can recover funds when the merchant or business is legitimate. But he emphasized limits: "These attacks often come from overseas, and they're mounted in a way that makes them virtually untraceable," he said, adding that by the time many complaints arrive, the funds are gone or the perpetrators are outside the AGO's jurisdiction.

Policy options and prevention: The AGO recommended focusing legislative attention on back‑end payment safeguards that slow or limit irreversible transfers (waiting periods, transaction limits or clearer warnings). Colgan said consumer education remains a priority and urged people to report suspected scams to the Attorney General’s consumer resource center and to other agencies such as the Department of Financial Institutions.

The committee exchanged questions with AGO staff about underreporting, definitions of "older adult" (the FTC generally uses 60+ but losses spike at 70+), and whether state‑level action can affect federally chartered banks. Colgan said state options are limited for federally chartered institutions but recommended exploring state action on cryptocurrency kiosks and other points of vulnerability.

What’s next: The presentation prompted interest from members about legislative and regulatory responses; no formal action or vote was taken at the work session.

View the Full Meeting & All Its Details

This article offers just a summary. Unlock complete video, transcripts, and insights as a Founder Member.

✓

Watch full, unedited meeting videos

✓

Search every word spoken in unlimited transcripts

✓

AI summaries & real-time alerts (all government levels)

✓

Permanent access to expanding government content

30-day money-back guarantee