Finance Committee reviews proposed Vermont NIIT; billers, thresholds and school construction funding debated

February 20, 2026 | Finance, SENATE, Committees, Legislative , Vermont

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

The Finance Committee on Feb. (date not specified) took a detailed briefing from Patrick Denton of the Joint Fiscal Office on a proposal to impose a state net investment income tax, sometimes described in the meeting as a "wealth proceeds" tax, and on options for dedicating the revenue to school construction.

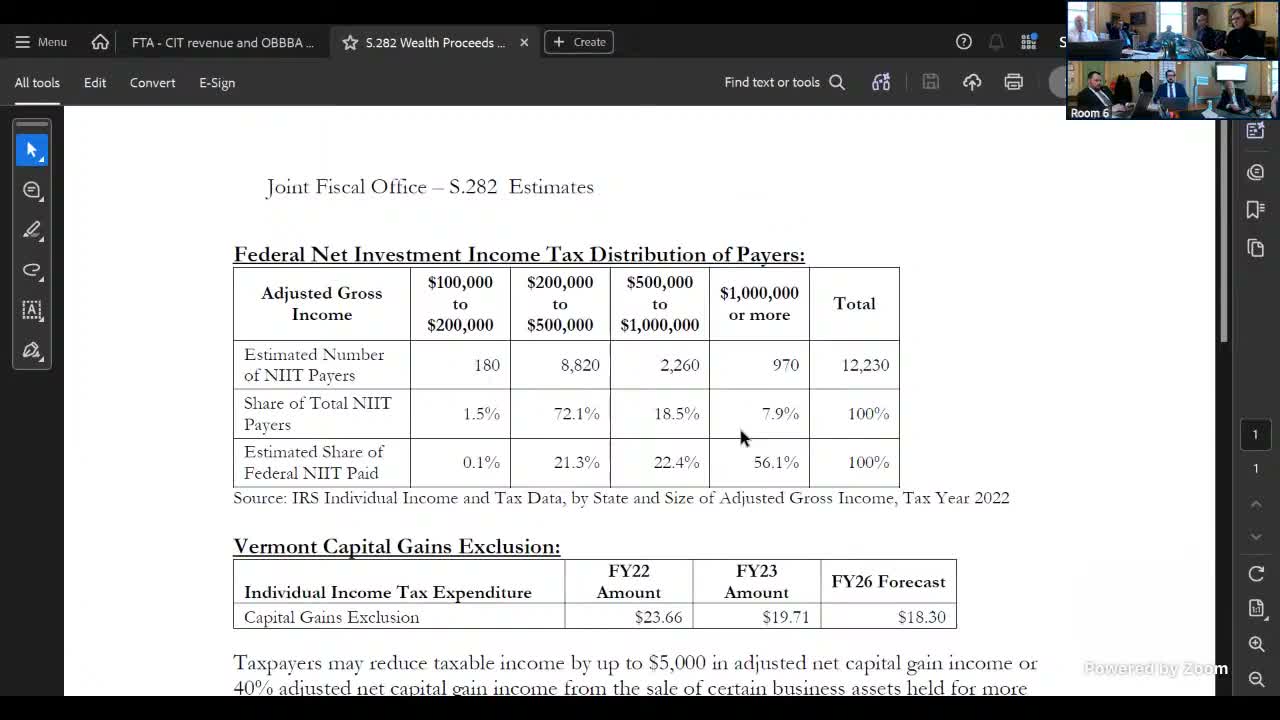

Denton summarized data from Verus (2022), saying, "So in Vermont, there's about 12,000 people who exceed those thresholds, have this investment income and are paying the federal net investment, income tax." He said revenue is concentrated among higher-income filers: taxpayers with adjusted gross income above $1 million provide a disproportionate share of receipts, and combining filers above $500,000 captures roughly 70–80% of expected receipts.

Staff presented several revenue scenarios. Denton said the expanded form of the proposal as currently drafted is estimated to yield "just shy of $60,000,000" in additional state revenue. Using the federal thresholds (the $200,000 starting point) produced an estimate of about $48,649,000, while raising the threshold to $500,000 would shrink the payer pool to roughly 3,200 filers and reduce revenue to an estimated $46–47 million, depending on which income categories are included.

Committee members pressed on how the bill’s proceeds would be used. The proposal discussed during the briefing suggested directing revenue toward school construction, but Denton cautioned that "there was intent language suggesting that, but there was no mechanism to, like, officially dedicate" the money to a special fund. Members said the treasurer’s office has raised concerns about pledging the state's full faith and credit for school debt and suggested using municipal bond bank structures with grants or other mechanisms to lower borrowing costs without creating an unconditional pledge.

Members and staff also flagged practical considerations for taxpayers and administrators: aligning state definitions with federal filing to simplify compliance; potential taxpayer behaviour changes if thresholds differ from federal rules; and the need for the Tax Department and the treasurer’s office to clarify implementation and bonding options.

The committee asked staff to return with more detailed scoring and legal/administrative guidance from tax department attorneys and the treasurer’s office; members suggested inviting witnesses such as Treasurer’s Office staff and Bob Donahue to discuss school construction mechanics. No formal vote or motion was recorded during the meeting.

Denton summarized data from Verus (2022), saying, "So in Vermont, there's about 12,000 people who exceed those thresholds, have this investment income and are paying the federal net investment, income tax." He said revenue is concentrated among higher-income filers: taxpayers with adjusted gross income above $1 million provide a disproportionate share of receipts, and combining filers above $500,000 captures roughly 70–80% of expected receipts.

Staff presented several revenue scenarios. Denton said the expanded form of the proposal as currently drafted is estimated to yield "just shy of $60,000,000" in additional state revenue. Using the federal thresholds (the $200,000 starting point) produced an estimate of about $48,649,000, while raising the threshold to $500,000 would shrink the payer pool to roughly 3,200 filers and reduce revenue to an estimated $46–47 million, depending on which income categories are included.

Committee members pressed on how the bill’s proceeds would be used. The proposal discussed during the briefing suggested directing revenue toward school construction, but Denton cautioned that "there was intent language suggesting that, but there was no mechanism to, like, officially dedicate" the money to a special fund. Members said the treasurer’s office has raised concerns about pledging the state's full faith and credit for school debt and suggested using municipal bond bank structures with grants or other mechanisms to lower borrowing costs without creating an unconditional pledge.

Members and staff also flagged practical considerations for taxpayers and administrators: aligning state definitions with federal filing to simplify compliance; potential taxpayer behaviour changes if thresholds differ from federal rules; and the need for the Tax Department and the treasurer’s office to clarify implementation and bonding options.

The committee asked staff to return with more detailed scoring and legal/administrative guidance from tax department attorneys and the treasurer’s office; members suggested inviting witnesses such as Treasurer’s Office staff and Bob Donahue to discuss school construction mechanics. No formal vote or motion was recorded during the meeting.

Don't Miss a Word: See the Full Meeting!

Go beyond summaries. Unlock every video, transcript, and key insight with a Founder Membership.

✓

Get instant access to full meeting videos

✓

Search and clip any phrase from complete transcripts

✓

Receive AI-powered summaries & custom alerts

✓

Enjoy lifetime, unrestricted access to government data

30-day money-back guarantee