Committee seeks details on capital gains exclusion, residency rules and NIIT administration

February 20, 2026 | Finance, SENATE, Committees, Legislative , Vermont

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

Committee members focused on implementation questions that could alter who pays a state NIIT and how much revenue it would raise.

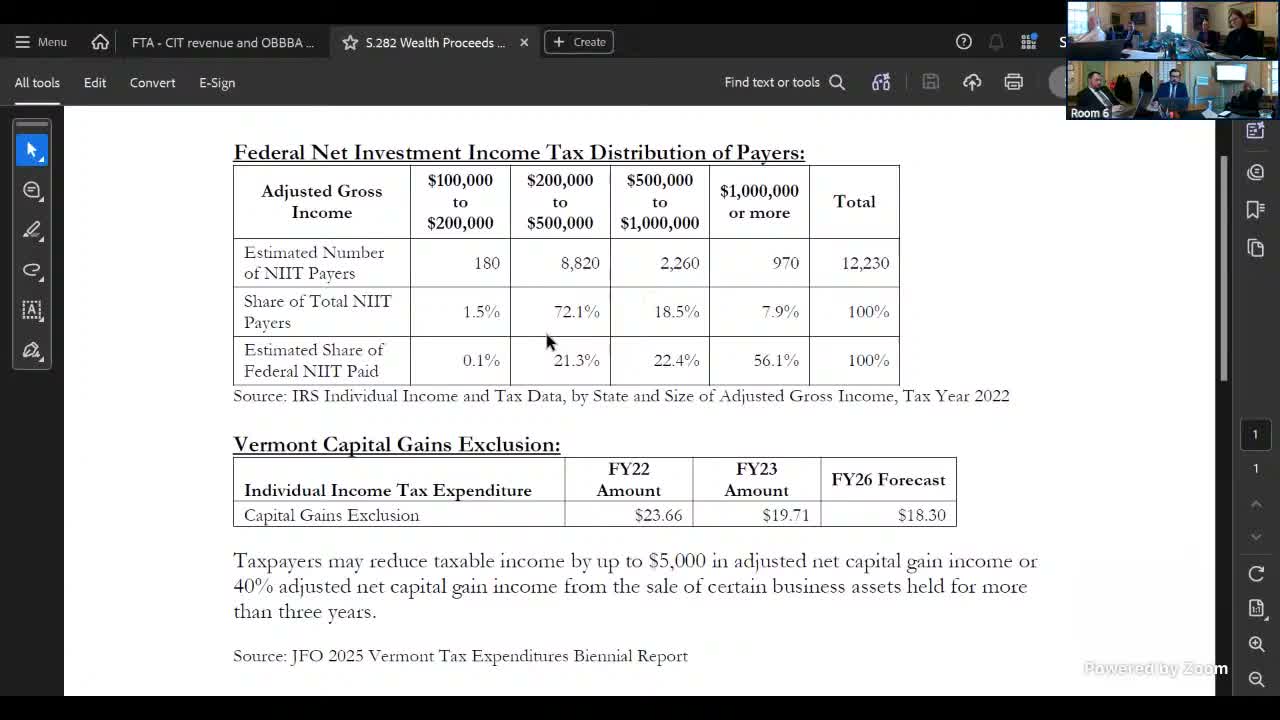

Patrick Denton told the committee the Vermont personal income tax currently includes a capital gains exclusion that can reduce taxable income by up to $5,000 and that the exclusion’s forecasted tax expenditure for FY26 is about $18 million. He also said "about a little less than 60% of the income that is captured by the NIIT, is from capital gains," and that would affect how a state tax performs and how taxpayers time sales.

Members asked whether the exclusion applies to business and farm sales, whether there is a holding-period requirement (Denton said he believed there may be a three‑year holding requirement and would confirm), and whether the state could exclude capital gains from a state NIIT while taxing other NIIT income types such as dividends, rental income and annuities. A committee member framed the policy choice this way: could the state "segregate capital gains out and only look at the other 4 types of NIT incomes that are more continual," which would change both revenue and taxpayer incentives.

Residency and apportionment questions were raised repeatedly. Members described scenarios (for example, a lifetime Vermont resident who moves to Florida and sells a Vermont-based business) and asked whether nonresident filing rules or credits would require a Vermont return. Staff said apportionment generally follows domicile rules and recommended seeking the Tax Department’s attorneys for definitive legal guidance.

The committee asked staff to return with clarified answers on the capital gains exclusion’s statutory text, any holding-period conditions, whether the tax can be administratively implemented to exclude capital gains, and how apportionment and nonresident filings would be handled. No implementation decision was made at this meeting.

Patrick Denton told the committee the Vermont personal income tax currently includes a capital gains exclusion that can reduce taxable income by up to $5,000 and that the exclusion’s forecasted tax expenditure for FY26 is about $18 million. He also said "about a little less than 60% of the income that is captured by the NIIT, is from capital gains," and that would affect how a state tax performs and how taxpayers time sales.

Members asked whether the exclusion applies to business and farm sales, whether there is a holding-period requirement (Denton said he believed there may be a three‑year holding requirement and would confirm), and whether the state could exclude capital gains from a state NIIT while taxing other NIIT income types such as dividends, rental income and annuities. A committee member framed the policy choice this way: could the state "segregate capital gains out and only look at the other 4 types of NIT incomes that are more continual," which would change both revenue and taxpayer incentives.

Residency and apportionment questions were raised repeatedly. Members described scenarios (for example, a lifetime Vermont resident who moves to Florida and sells a Vermont-based business) and asked whether nonresident filing rules or credits would require a Vermont return. Staff said apportionment generally follows domicile rules and recommended seeking the Tax Department’s attorneys for definitive legal guidance.

The committee asked staff to return with clarified answers on the capital gains exclusion’s statutory text, any holding-period conditions, whether the tax can be administratively implemented to exclude capital gains, and how apportionment and nonresident filings would be handled. No implementation decision was made at this meeting.

View the Full Meeting & All Its Details

This article offers just a summary. Unlock complete video, transcripts, and insights as a Founder Member.

✓

Watch full, unedited meeting videos

✓

Search every word spoken in unlimited transcripts

✓

AI summaries & real-time alerts (all government levels)

✓

Permanent access to expanding government content

30-day money-back guarantee