Harnett County updates mobile‑home assessment schedule; some manufactured homes get large value increases

February 19, 2026 | Harnett County, North Carolina

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

Speaker 4, a presenter for the Harnett County Tax Department, told the audience the county had revised personal-property schedule values for manufactured/mobile homes to address inequities created when those schedules had not been updated since 1998.

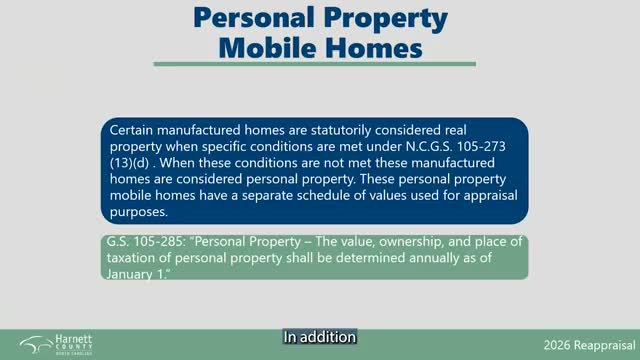

"This classification is based on North Carolina general statute 105-273," Speaker 4 said while explaining that to be classified as real property, a manufactured home must meet conditions such as removal of hitch wheels and placement on a permanent foundation and that the land be owned by the same owner as the home.

Staff said the older personal-property schedule relied primarily on age and size and had not been revised since 1998, while real-property manufactured homes were being reassessed on a four-year schedule. That discrepancy, combined with strong growth in mobile-home sales in recent years, produced disparities in assessed values that the new schedule seeks to correct.

Speaker 4 presented four example calculations showing how values will change under the new schedule: an older single‑wide example moving to $33,281 for 2026; a new single‑wide example to $62,432; a used double‑wide example to $64,997; and a new double‑wide example to $129,260. The presentation included market sales used for comparison and noted the county applied factors similar to real-property assessments—size, year manufactured, quality grade, condition, and mobile‑home type—citing N.C. Gen. Stat. § 105-317.1 as the statutory basis for the approach.

Staff emphasized that personal-property appeal forms for manufactured homes will be available online, in person, or by mail and that taxpayers should file a separate form for each mobile home they plan to appeal. The presentation included guidance on supporting documentation (photos, condition details, sale comparables, or a fee appraisal from 2024–25) and reiterated that appeals must be based on market value as of Jan. 1, 2026.

The county said the revised schedule is intended to produce fairer, more consistent assessments across property classes and townships; residents with questions were directed to the tax office for assistance.

"This classification is based on North Carolina general statute 105-273," Speaker 4 said while explaining that to be classified as real property, a manufactured home must meet conditions such as removal of hitch wheels and placement on a permanent foundation and that the land be owned by the same owner as the home.

Staff said the older personal-property schedule relied primarily on age and size and had not been revised since 1998, while real-property manufactured homes were being reassessed on a four-year schedule. That discrepancy, combined with strong growth in mobile-home sales in recent years, produced disparities in assessed values that the new schedule seeks to correct.

Speaker 4 presented four example calculations showing how values will change under the new schedule: an older single‑wide example moving to $33,281 for 2026; a new single‑wide example to $62,432; a used double‑wide example to $64,997; and a new double‑wide example to $129,260. The presentation included market sales used for comparison and noted the county applied factors similar to real-property assessments—size, year manufactured, quality grade, condition, and mobile‑home type—citing N.C. Gen. Stat. § 105-317.1 as the statutory basis for the approach.

Staff emphasized that personal-property appeal forms for manufactured homes will be available online, in person, or by mail and that taxpayers should file a separate form for each mobile home they plan to appeal. The presentation included guidance on supporting documentation (photos, condition details, sale comparables, or a fee appraisal from 2024–25) and reiterated that appeals must be based on market value as of Jan. 1, 2026.

The county said the revised schedule is intended to produce fairer, more consistent assessments across property classes and townships; residents with questions were directed to the tax office for assistance.

Don't Miss a Word: See the Full Meeting!

Go beyond summaries. Unlock every video, transcript, and key insight with a Founder Membership.

✓

Get instant access to full meeting videos

✓

Search and clip any phrase from complete transcripts

✓

Receive AI-powered summaries & custom alerts

✓

Enjoy lifetime, unrestricted access to government data

30-day money-back guarantee