Experts tell Vermont committee reversing section 174 would ease tax pain for grant-funded firms

February 06, 2026 | Ways & Means, HOUSE OF REPRESENTATIVES, Committees, Legislative , Vermont

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

Tax experts and business advocates told the Ways and Means Committee on Feb. 5 that restoring immediate expensing for research and development costs could materially improve cash flow for companies that rely on grants or make heavy R&D investments.

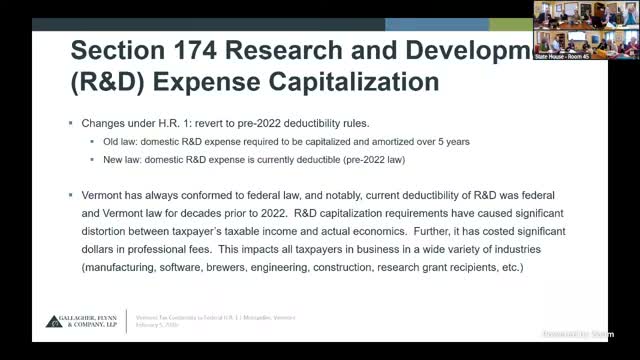

"HR 1 essentially reverses this section 174 capitalization and says that we're allowed to go back to the rules for federal purposes that, allow immediate expensing of R and D expenditure," said Mike Hackett, a tax partner at Gallagher Flynn. Hackett illustrated with an example in which a company with $1 million of revenue and $500,000 in R&D wages would be moved from a tax loss to a taxable position under the TCJA-era amortization rules, a distortion he said HR1 would correct for many firms.

Hackett and other witnesses described the provision's particular impact on entities funded by federal research grants. Those organizations typically operate on cost-plus arrangements; when R&D spending must be amortized rather than expensed immediately, the organizations may face tax liabilities they cannot pay from the grant funds, forcing them to borrow or jeopardize operations.

Experts also noted practical caveats: if Vermont delays conformity, taxpayers may not be able to amend prior federal-year filings for Vermont purposes and could lose deductions on 2025 Vermont returns without legislative fixes. The committee sought clarification about who would be eligible for small-taxpayer relief under HR1; Hackett said the federal small-taxpayer threshold in HR1 is about $31 million in gross receipts and that many Vermont companies fall within that range.

The hearing produced no decision; members indicated the R&D expensing question will be a core item in the committee's follow-up fiscal work and legislative drafting.

"HR 1 essentially reverses this section 174 capitalization and says that we're allowed to go back to the rules for federal purposes that, allow immediate expensing of R and D expenditure," said Mike Hackett, a tax partner at Gallagher Flynn. Hackett illustrated with an example in which a company with $1 million of revenue and $500,000 in R&D wages would be moved from a tax loss to a taxable position under the TCJA-era amortization rules, a distortion he said HR1 would correct for many firms.

Hackett and other witnesses described the provision's particular impact on entities funded by federal research grants. Those organizations typically operate on cost-plus arrangements; when R&D spending must be amortized rather than expensed immediately, the organizations may face tax liabilities they cannot pay from the grant funds, forcing them to borrow or jeopardize operations.

Experts also noted practical caveats: if Vermont delays conformity, taxpayers may not be able to amend prior federal-year filings for Vermont purposes and could lose deductions on 2025 Vermont returns without legislative fixes. The committee sought clarification about who would be eligible for small-taxpayer relief under HR1; Hackett said the federal small-taxpayer threshold in HR1 is about $31 million in gross receipts and that many Vermont companies fall within that range.

The hearing produced no decision; members indicated the R&D expensing question will be a core item in the committee's follow-up fiscal work and legislative drafting.

Don't Miss a Word: See the Full Meeting!

Go beyond summaries. Unlock every video, transcript, and key insight with a Founder Membership.

✓

Get instant access to full meeting videos

✓

Search and clip any phrase from complete transcripts

✓

Receive AI-powered summaries & custom alerts

✓

Enjoy lifetime, unrestricted access to government data

30-day money-back guarantee