Committee reviews S.238: 2% rooms surcharge and 1¢/oz beverage excise to seed housing fund

February 06, 2026 | Economic Development, Housing & General Affairs, SENATE, Committees, Legislative , Vermont

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

Madam Chair opened a committee hearing on S.238 on Feb. 6, describing the bill as a first attempt to secure recurring revenue for housing development by imposing a 2% surcharge on the state rooms tax and a 1¢ per‑ounce sugar‑sweetened beverage excise to backfill the education fund.

The chair said Vermont’s housing goals — 7,500 new units a year — will not be met without sustained funding, noting an internal estimate that about 4,000 of those units will require state or state‑enabled financial support. "If we're gonna continue to build housing ... we have to identify an additional source of revenue," the chair said.

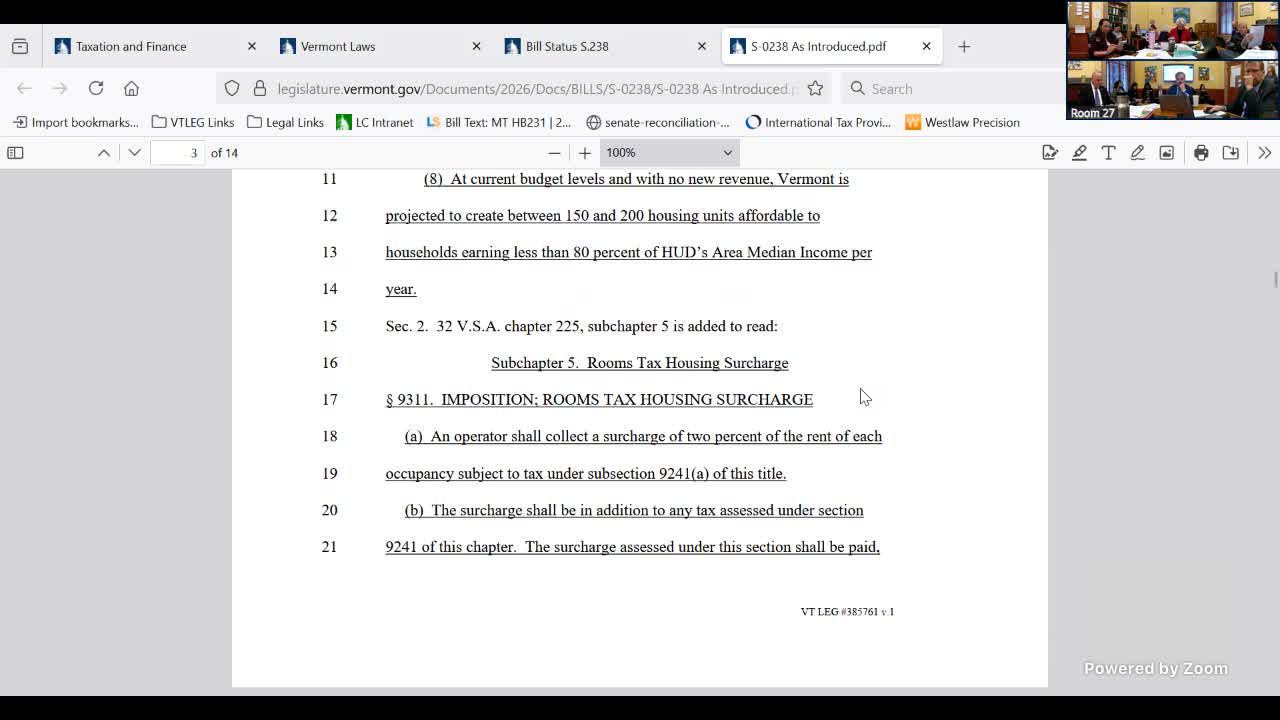

Kirby Dean, legislative counsel, gave a section‑by‑section overview. He said section 2 would add a 2% surcharge to the existing rooms tax base (hotels, bed‑and‑breakfasts and short‑term rentals). "Everything that the rooms tax applies to would be applied for this instance," Dean said. Section 3 would impose a 1¢/ounce excise on sugar‑sweetened beverages, collected from distributors, and sections 4–6 would create the Housing Investment Special Fund and authorize initial appropriations from that fund.

Ted of the Joint Fiscal Office summarized revenue modeling and cautioned the estimates were conservative and implementation details remain. He estimated the 2% surcharge would generate about $16.4 million in fiscal year 2027 under a partial‑year assumption and about $20 million in a full year; combined with reallocated short‑term‑rental surcharge proceeds, the Housing Investment Special Fund would see an estimated $20.8 million in FY27 and about $29.6 million in FY28 under the scenarios presented. Ted noted his team factored in a demand elasticity assumption roughly in the -0.7 range and warned the beverage excise — a fixed‑amount tax — would not grow with inflation and could face cross‑border purchasing effects.

The bill would direct the General Assembly to appropriate funds from the new special fund for specific housing purposes; Dean noted the introduced text includes a $5 million fiscal‑year appropriation to the Department of Housing and Community Development for its first year and lists intended uses such as funding affordable and supportive housing development.

Committee members raised competitiveness questions — how added room taxes would stack with local taxes (including Burlington’s different tax structure) and how tourism‑sensitive markets might respond. Members also asked staff to provide jurisdictional comparisons and more granular short‑term rental revenue data for places such as Burlington before reallocating STR revenue from the Education Fund.

The committee set follow‑up work: staff will supply more detailed fiscal comparisons and implementation considerations, and housing partners will return with regional cost‑and‑capacity analyses.

The hearing recessed for a break and expected to continue later in the day.

The chair said Vermont’s housing goals — 7,500 new units a year — will not be met without sustained funding, noting an internal estimate that about 4,000 of those units will require state or state‑enabled financial support. "If we're gonna continue to build housing ... we have to identify an additional source of revenue," the chair said.

Kirby Dean, legislative counsel, gave a section‑by‑section overview. He said section 2 would add a 2% surcharge to the existing rooms tax base (hotels, bed‑and‑breakfasts and short‑term rentals). "Everything that the rooms tax applies to would be applied for this instance," Dean said. Section 3 would impose a 1¢/ounce excise on sugar‑sweetened beverages, collected from distributors, and sections 4–6 would create the Housing Investment Special Fund and authorize initial appropriations from that fund.

Ted of the Joint Fiscal Office summarized revenue modeling and cautioned the estimates were conservative and implementation details remain. He estimated the 2% surcharge would generate about $16.4 million in fiscal year 2027 under a partial‑year assumption and about $20 million in a full year; combined with reallocated short‑term‑rental surcharge proceeds, the Housing Investment Special Fund would see an estimated $20.8 million in FY27 and about $29.6 million in FY28 under the scenarios presented. Ted noted his team factored in a demand elasticity assumption roughly in the -0.7 range and warned the beverage excise — a fixed‑amount tax — would not grow with inflation and could face cross‑border purchasing effects.

The bill would direct the General Assembly to appropriate funds from the new special fund for specific housing purposes; Dean noted the introduced text includes a $5 million fiscal‑year appropriation to the Department of Housing and Community Development for its first year and lists intended uses such as funding affordable and supportive housing development.

Committee members raised competitiveness questions — how added room taxes would stack with local taxes (including Burlington’s different tax structure) and how tourism‑sensitive markets might respond. Members also asked staff to provide jurisdictional comparisons and more granular short‑term rental revenue data for places such as Burlington before reallocating STR revenue from the Education Fund.

The committee set follow‑up work: staff will supply more detailed fiscal comparisons and implementation considerations, and housing partners will return with regional cost‑and‑capacity analyses.

The hearing recessed for a break and expected to continue later in the day.

View the Full Meeting & All Its Details

This article offers just a summary. Unlock complete video, transcripts, and insights as a Founder Member.

✓

Watch full, unedited meeting videos

✓

Search every word spoken in unlimited transcripts

✓

AI summaries & real-time alerts (all government levels)

✓

Permanent access to expanding government content

30-day money-back guarantee