Maryland labor secretary flags long-term solvency risks, urges consideration of taxable wage-base changes

February 05, 2026 | Economic Matters Committee, HOUSE OF REPRESENTATIVES, Committees, Legislative, Maryland

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

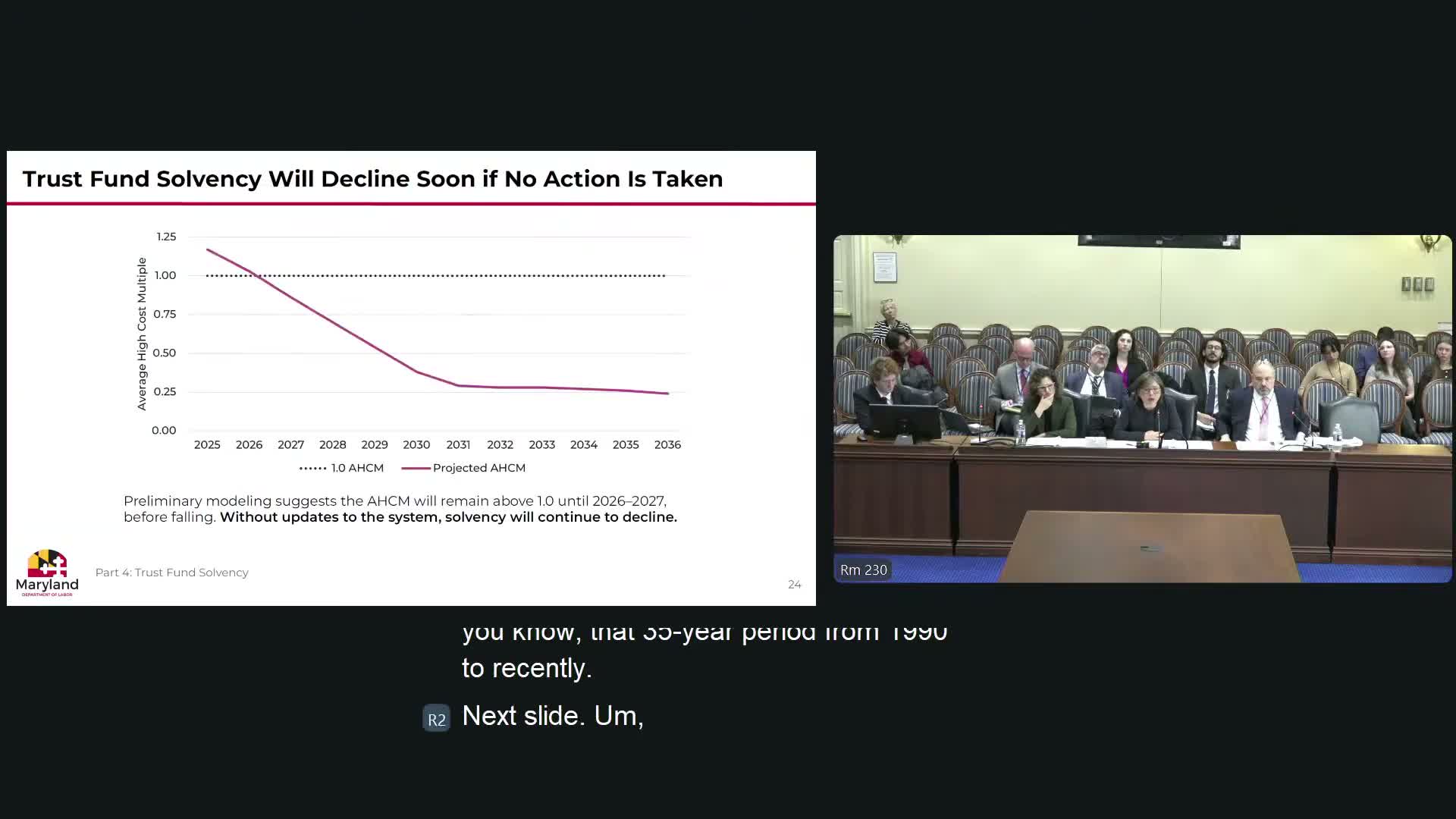

Secretary Wu told the Economic Matters Committee on Feb. 4 that while Maryland's unemployment insurance trust fund is currently above the average high-cost multiplier (AHCM) solvency benchmark, long-term pressures could shrink balances unless structural changes are made.

Wu explained that the AHCM is a benchmark indicating whether a state has enough in its trust fund to pay a year of benefits in a typical recession; being above 1 preserves the state's ability to borrow interest-free from the federal government during severe drawdowns. "As long as you have been recently maintaining good solvency, you can go to the federal government, and they will back up your trust fund with an interest free loan," she said.

Why it matters: The department's projections, based on U.S. Department of Labor modeling, show solvency declining over time if no action is taken. Structural pressures include rising average weekly benefits (Secretary cited a growing share of claimants receiving the $430 maximum), a fixed taxable wage base of $8,500 and wage inflation pushing more claimants toward the benefit ceiling.

Key numbers and mechanics: Wu said Maryland's taxable wage base is $8,500 ("40 fourth in the nation," in her phrasing) and was last changed in 1992. She noted regional peers such as Pennsylvania and Delaware have higher wage bases and said indexing or raising the base spreads contributions over time, avoiding large countercyclical tax spikes in recessions. The presentation showed how tax "tables" move employers to higher rates when trust funds decline, which typically happens in downturns.

Committee questions and context: Delegates asked about the practical impact of indexing the base and whether employers would pay more; Wu said the tax rate structure could remain the same but be applied to a larger taxable wage base, increasing employer contributions on higher-paid employees. Committee members also raised concerns about protecting trust-fund dollars from other uses; Wu said UI trust funds are restricted by federal-state partnership rules and cannot be diverted to unrelated programs.

What happens next: Committee members signaled intent to consider legislation on the taxable wage base this session. The department said it will provide additional modeling on indexing and fiscal impacts and work with the committee on any proposed statutory changes.

Wu explained that the AHCM is a benchmark indicating whether a state has enough in its trust fund to pay a year of benefits in a typical recession; being above 1 preserves the state's ability to borrow interest-free from the federal government during severe drawdowns. "As long as you have been recently maintaining good solvency, you can go to the federal government, and they will back up your trust fund with an interest free loan," she said.

Why it matters: The department's projections, based on U.S. Department of Labor modeling, show solvency declining over time if no action is taken. Structural pressures include rising average weekly benefits (Secretary cited a growing share of claimants receiving the $430 maximum), a fixed taxable wage base of $8,500 and wage inflation pushing more claimants toward the benefit ceiling.

Key numbers and mechanics: Wu said Maryland's taxable wage base is $8,500 ("40 fourth in the nation," in her phrasing) and was last changed in 1992. She noted regional peers such as Pennsylvania and Delaware have higher wage bases and said indexing or raising the base spreads contributions over time, avoiding large countercyclical tax spikes in recessions. The presentation showed how tax "tables" move employers to higher rates when trust funds decline, which typically happens in downturns.

Committee questions and context: Delegates asked about the practical impact of indexing the base and whether employers would pay more; Wu said the tax rate structure could remain the same but be applied to a larger taxable wage base, increasing employer contributions on higher-paid employees. Committee members also raised concerns about protecting trust-fund dollars from other uses; Wu said UI trust funds are restricted by federal-state partnership rules and cannot be diverted to unrelated programs.

What happens next: Committee members signaled intent to consider legislation on the taxable wage base this session. The department said it will provide additional modeling on indexing and fiscal impacts and work with the committee on any proposed statutory changes.

View the Full Meeting & All Its Details

This article offers just a summary. Unlock complete video, transcripts, and insights as a Founder Member.

✓

Watch full, unedited meeting videos

✓

Search every word spoken in unlimited transcripts

✓

AI summaries & real-time alerts (all government levels)

✓

Permanent access to expanding government content

30-day money-back guarantee