Davenport City presents proposed FY2027 budget, proposes small levy drop and warns state caps could strain services

January 31, 2026 | Davenport City, Scott County, Iowa

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

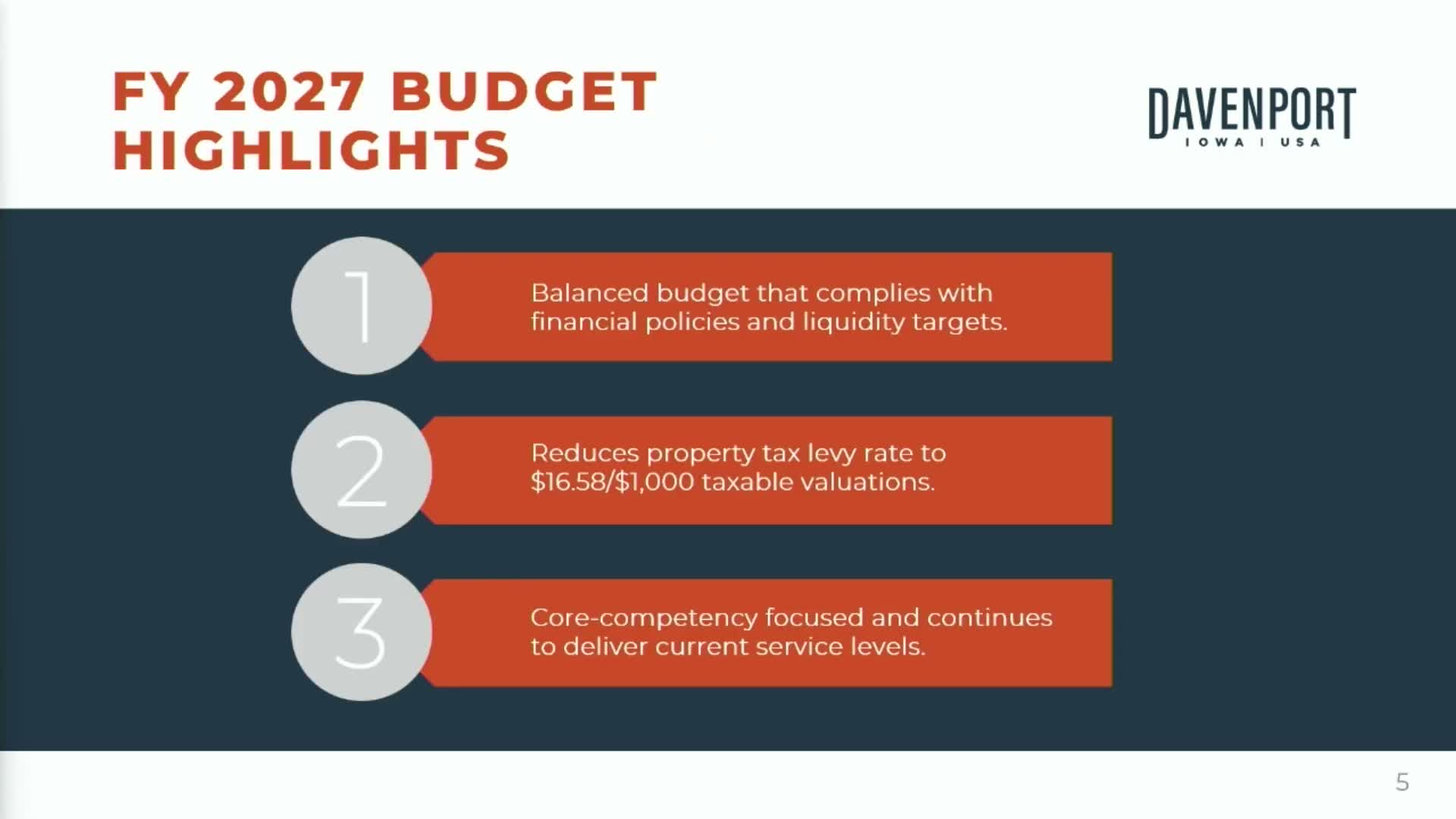

Unidentified Presenter (Speaker 4) presented the city's proposed fiscal year 2027 budget, saying it is structurally balanced and continues current service levels while proposing a small reduction in the total property-tax levy. Speaker 4 said the combined general fund levy is proposed at $8.20 and the total levy would fall just shy of $16.58 per $1,000 taxable valuation, down from $16.61.

The presentation framed reserve policy as central to fiscal health. Speaker 4 said the city's unassigned operating general fund reserve sits at about 25% of expenditures, a level the finance presenter and council members said they prefer to keep. Speaker 2 and others warned that a state-level proposal to cap local revenue growth (discussed informally during the meeting as a 2% cap) and separate proposals to lower unassigned fund balance expectations to 10% would be at odds with guidance from the Government Finance Officers Association and could put pressure on bond ratings and future borrowing costs.

Speaker 2 urged residents to contact state legislators about any proposed caps. In the presentation Speaker 4 noted: "I find that concerning" when describing a possible reduction of unassigned fund balance requirements to 10% and said weaker reserves could translate into higher interest costs if ratings fall.

Staff walked council through the mechanics of property tax calculation under recent state law changes (see House File 718), showing that non-TIF taxable value growth of 5.73% and the statutory rollback/tiers produced a 16-cent reduction in the combined general fund levy compared with the prior year. Speaker 6 and others asked clarifying questions about how assessed-value growth translates into revenue and how the state formulas affect local tax rates; staff responded that the non-TIF growth figure reflects assessment changes rather than a direct expansion of new taxable parcels.

Council members asked for follow-up materials and additional detail on any potential effects if the state finalizes limits on local revenue growth. The city intends to continue the workshop series, bring more detail at the Feb. 3 management update and the February capital meeting, and adopt the final FY2027 budget in April if the council approves.

The presentation framed reserve policy as central to fiscal health. Speaker 4 said the city's unassigned operating general fund reserve sits at about 25% of expenditures, a level the finance presenter and council members said they prefer to keep. Speaker 2 and others warned that a state-level proposal to cap local revenue growth (discussed informally during the meeting as a 2% cap) and separate proposals to lower unassigned fund balance expectations to 10% would be at odds with guidance from the Government Finance Officers Association and could put pressure on bond ratings and future borrowing costs.

Speaker 2 urged residents to contact state legislators about any proposed caps. In the presentation Speaker 4 noted: "I find that concerning" when describing a possible reduction of unassigned fund balance requirements to 10% and said weaker reserves could translate into higher interest costs if ratings fall.

Staff walked council through the mechanics of property tax calculation under recent state law changes (see House File 718), showing that non-TIF taxable value growth of 5.73% and the statutory rollback/tiers produced a 16-cent reduction in the combined general fund levy compared with the prior year. Speaker 6 and others asked clarifying questions about how assessed-value growth translates into revenue and how the state formulas affect local tax rates; staff responded that the non-TIF growth figure reflects assessment changes rather than a direct expansion of new taxable parcels.

Council members asked for follow-up materials and additional detail on any potential effects if the state finalizes limits on local revenue growth. The city intends to continue the workshop series, bring more detail at the Feb. 3 management update and the February capital meeting, and adopt the final FY2027 budget in April if the council approves.

View the Full Meeting & All Its Details

This article offers just a summary. Unlock complete video, transcripts, and insights as a Founder Member.

✓

Watch full, unedited meeting videos

✓

Search every word spoken in unlimited transcripts

✓

AI summaries & real-time alerts (all government levels)

✓

Permanent access to expanding government content

30-day money-back guarantee