Assembly frames repayment plan after audit finds $5.4M central‑treasury shortfall tied to school district

January 23, 2026 | Ketchikan Gateway Borough, Alaska

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

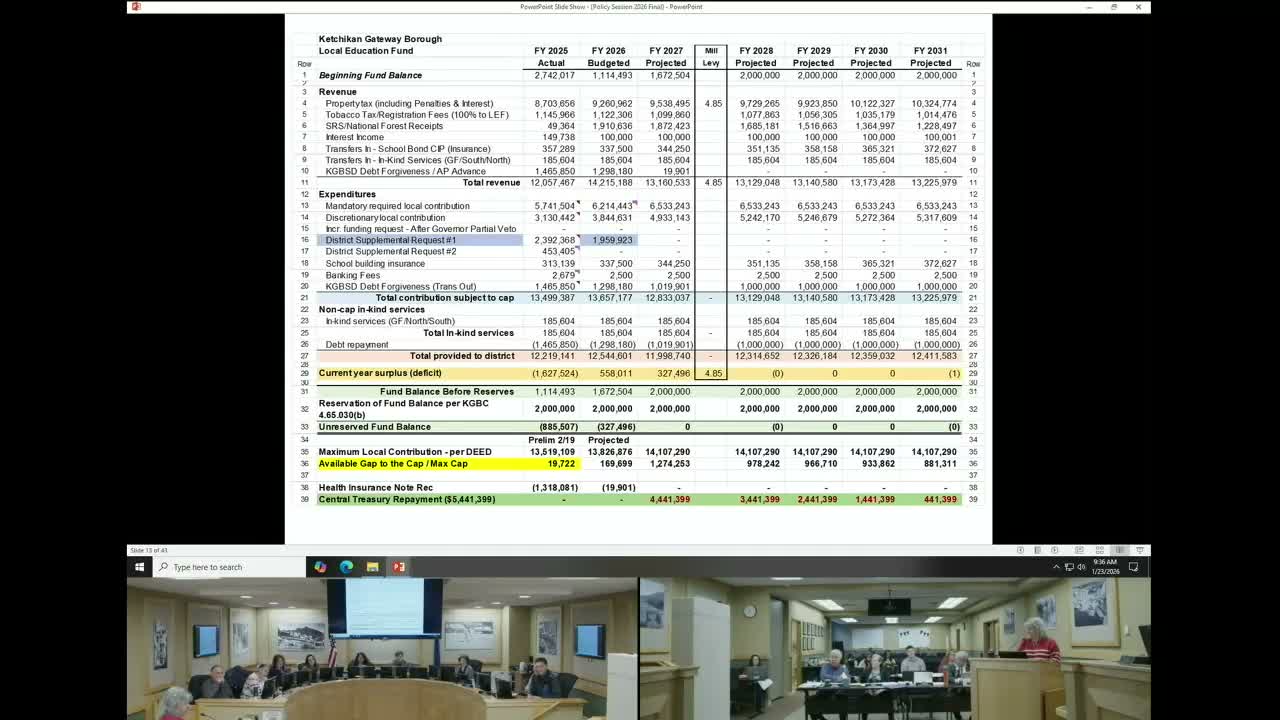

The Assembly spent extensive time on Jan. 23 examining a $5.4 million central‑treasury payable the borough identified during an audit of the Ketchikan Gateway Borough School District. Managers and finance staff told the Assembly the payable represents advances drawn against future state disbursements and that converting the amount into a structured loan would be preferable to writing it off.

Manager remarks and staff analysis showed the payable emerged from central‑treasury transactions rather than routine, approved transfers. Assembly members expressed concern about the district’s cash flow and the fiscal risk to borough taxpayers if the payable were simply forgiven. After debate, the Assembly gave staff direction to treat the amount as a repayable obligation and approved assumptions that include charging interest on the district’s outstanding obligation at a rate comparable to borough service‑district financing. The Assembly also directed staff to prepare a repayment schedule and, during the FY27 appropriation discussions, accepted a staff‑suggested $1,000,000 annual contribution as part of debt recovery and ultimately voted to structure a multi‑year repayment to recover the identified $5.4 million; members settled on a three‑year plan as staff returns proposals (vote to include three‑year repayment among assumptions passed unanimously).

Key clarifications: staff said the $5.4 million is being held (sequestered) and that releasing even a portion would require up‑to‑date cash‑flow projections and conditions in a memorandum of agreement. The manager emphasized legal and practical limits, noting that the borough must avoid creating a new liability by failing to comply with vendor or payroll obligations.

Why it matters: the payable touches the borough’s balance sheet and the LEF, which funds local contributions to the school district. How the parties resolve repayment affects services and budgeting for both the borough and the district and sets precedent for treatment of interfund liabilities.

What’s next: staff will include the repayment assumptions and interest policy in the LEF appropriation work and return draft language for the Assembly to consider. The borough attorney intends to provide legal analysis on interest application and any statutory constraints.

Representative quotes: Assemblymember Bowling said charging interest is not punitive: “If that money hadn’t gone to those expenses, it would be earning interest for the borough population.” Manager (unnamed) explained the central‑treasury mechanics with an example of advances that must be repaid: “So that’s what happened with the central treasury...the school district owes the borough the money.”

The Assembly also asked staff to seek the school district’s updated cash‑flow analysis before releasing any sequestered funds.

Manager remarks and staff analysis showed the payable emerged from central‑treasury transactions rather than routine, approved transfers. Assembly members expressed concern about the district’s cash flow and the fiscal risk to borough taxpayers if the payable were simply forgiven. After debate, the Assembly gave staff direction to treat the amount as a repayable obligation and approved assumptions that include charging interest on the district’s outstanding obligation at a rate comparable to borough service‑district financing. The Assembly also directed staff to prepare a repayment schedule and, during the FY27 appropriation discussions, accepted a staff‑suggested $1,000,000 annual contribution as part of debt recovery and ultimately voted to structure a multi‑year repayment to recover the identified $5.4 million; members settled on a three‑year plan as staff returns proposals (vote to include three‑year repayment among assumptions passed unanimously).

Key clarifications: staff said the $5.4 million is being held (sequestered) and that releasing even a portion would require up‑to‑date cash‑flow projections and conditions in a memorandum of agreement. The manager emphasized legal and practical limits, noting that the borough must avoid creating a new liability by failing to comply with vendor or payroll obligations.

Why it matters: the payable touches the borough’s balance sheet and the LEF, which funds local contributions to the school district. How the parties resolve repayment affects services and budgeting for both the borough and the district and sets precedent for treatment of interfund liabilities.

What’s next: staff will include the repayment assumptions and interest policy in the LEF appropriation work and return draft language for the Assembly to consider. The borough attorney intends to provide legal analysis on interest application and any statutory constraints.

Representative quotes: Assemblymember Bowling said charging interest is not punitive: “If that money hadn’t gone to those expenses, it would be earning interest for the borough population.” Manager (unnamed) explained the central‑treasury mechanics with an example of advances that must be repaid: “So that’s what happened with the central treasury...the school district owes the borough the money.”

The Assembly also asked staff to seek the school district’s updated cash‑flow analysis before releasing any sequestered funds.

Don't Miss a Word: See the Full Meeting!

Go beyond summaries. Unlock every video, transcript, and key insight with a Founder Membership.

✓

Get instant access to full meeting videos

✓

Search and clip any phrase from complete transcripts

✓

Receive AI-powered summaries & custom alerts

✓

Enjoy lifetime, unrestricted access to government data

30-day money-back guarantee