Committee reviews changes to machinery-and-equipment investment tax credit, including partial refundability

January 30, 2026 | Finance, SENATE, Committees, Legislative , Vermont

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

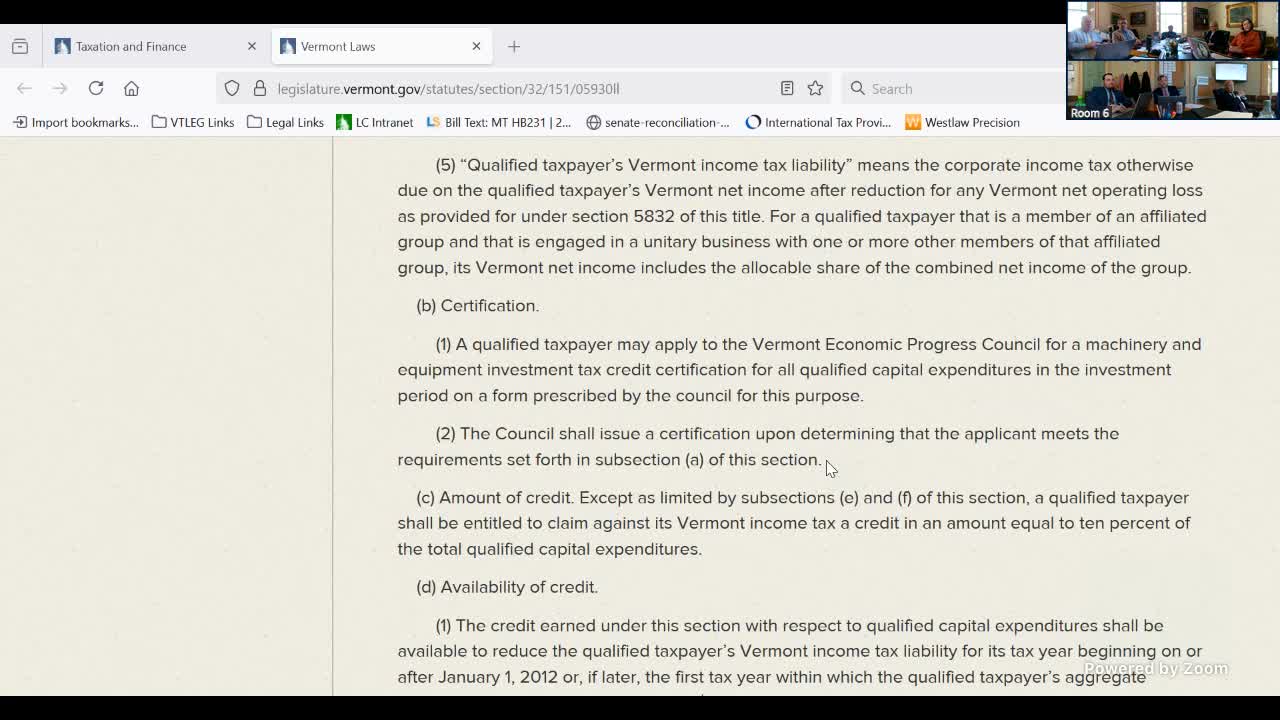

Legislative counsel briefed the Senate Finance Committee on proposed changes to the machinery-and-equipment investment tax credit, explaining the draft would (1) extend the statutory investment period, (2) broaden the definition of qualified expenditures, and (3) remove a statutory limit that currently prevents the credit from reducing a taxpayer’s Vermont income tax liability below 20% of tax due.

Under current law the credit cannot reduce corporate income tax liability by more than 80% in a single year, which prevents refunds. The proposal removes that 80% cap and allows a taxpayer to elect a refund of up to $500,000 of excess credit in a tax year; any remaining credit could still be carried forward under existing carryforward rules.

Committee members discussed how (and whether) the credit has been used historically, how corporate apportionment and the 2022 corporate tax changes affected whether affected companies pay Vermont corporate income tax, and whether the credit’s certification/administration process requires additional agency (JFO/Tax Department) review. Staff noted the statute resides under 32 VSA §5930l and related credit provisions.

No final committee action was taken on Jan. 30; committee members asked for fiscal impact review from JFO and the Department of Taxes before proceeding.

Under current law the credit cannot reduce corporate income tax liability by more than 80% in a single year, which prevents refunds. The proposal removes that 80% cap and allows a taxpayer to elect a refund of up to $500,000 of excess credit in a tax year; any remaining credit could still be carried forward under existing carryforward rules.

Committee members discussed how (and whether) the credit has been used historically, how corporate apportionment and the 2022 corporate tax changes affected whether affected companies pay Vermont corporate income tax, and whether the credit’s certification/administration process requires additional agency (JFO/Tax Department) review. Staff noted the statute resides under 32 VSA §5930l and related credit provisions.

No final committee action was taken on Jan. 30; committee members asked for fiscal impact review from JFO and the Department of Taxes before proceeding.

View the Full Meeting & All Its Details

This article offers just a summary. Unlock complete video, transcripts, and insights as a Founder Member.

✓

Watch full, unedited meeting videos

✓

Search every word spoken in unlimited transcripts

✓

AI summaries & real-time alerts (all government levels)

✓

Permanent access to expanding government content

30-day money-back guarantee