Vermont Ways & Means reviews tax department plan to implement Act 73's new property-tax classes

January 14, 2026 | Ways & Means, HOUSE OF REPRESENTATIVES, Committees, Legislative , Vermont

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

Jake Bellman, a tax department official, told the House Ways & Means Committee on Jan. 3 that Act 73 creates a new "nonhomestead residential" property class aimed at second homes and short-term rentals and laid out the administrative work required to make the law operational by fiscal 2029.

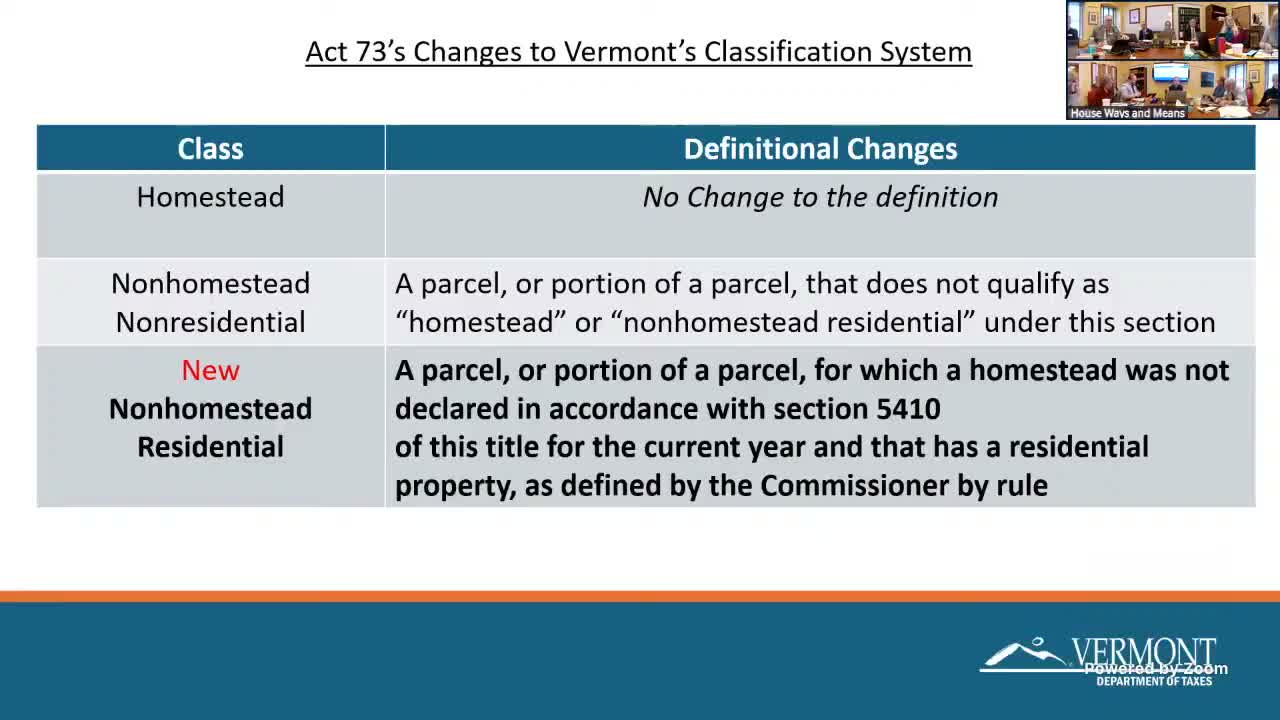

The report and presentation summarized how Act 73 changes Vermont's two-class system (homestead and nonhomestead) by adding the new class and moving to a statewide rate structure in which class-specific multipliers would be applied to a statewide base rate. "A new classification was introduced in act 73," Bellman said, and "rates are going to be uniform statewide," while the General Assembly could set multipliers annually.

Why it matters: the shift will change which property owners pay more, and will require extensive new data and municipal work. Bellman estimated the tax department will need to process "about a 173,000 homesteads" and "tens of thousands more" dwelling-use attestations, create or revise tax forms (a new dwelling-use attestation to replace the homestead declaration), and ensure towns can identify individual dwelling units by square footage and consistent identifiers.

Key implementation constraints include statutory dependencies and timing: new school district boundaries must be enacted by Jan. 1, 2027 for the mechanism to proceed, and multipliers will need to be set by July 1, 2028 to be effective for FY2029. Bellman called the statutory timeline "tight" and described the implementation as "doubly contingent" on those and other steps.

Committee members pressed for detail on several operational questions that remain unresolved in the report. Those include how to exclude long-term rentals from the new nonhomestead residential class, how to determine whether seasonal properties ("camps") are "fit for year-round application," whether municipalities can rely on external datasets (for example 9-1-1 records or landlord certificates) to locate dwelling units, and how land value should be apportioned when a parcel contains both residential and commercial uses. Bellman said some external datasets are imperfect and that towns will likely need to play a central role in verification.

Members also raised equity and enforcement concerns. Bellman noted Act 73 contains a default rule that would place units that appear fit for year-round habitation into the nonhomestead residential class unless an owner attests otherwise; he confirmed the default is deliberately adverse to encourage accurate reporting. The committee discussed penalties, appeals and whether to rely on the default rate as an incentive rather than expanding statutory fines.

The presentation included practical examples that highlight borderline and recurring cases: a single-family home converted to short-term rental; owner-occupied duplexes where one unit is vacant or periodically used by family; mixed commercial-residential buildings (a pottery studio with an apartment above); four-unit buildings with mixed short- and long-term rentals; and second homes with large outbuildings used commercially. For each example Bellman outlined how the dwelling-use attestation, square-footage apportionment and town records would determine classification and tax apportionment.

Next steps: the committee asked staff to draft decision points and a clear timetable. Chair Kornheiser asked Kirby Keaton to work with Julia Richter (JFO) and Bellman to produce a detailed timeline of decisions and statutory changes required over the next three years. The committee will revisit the decision tree and technical refinements in future meetings.

The committee did not take formal votes during this hearing. Members left several legislative questions unresolved (definitions of dwelling unit, land-value apportionment, precise penalty language) that staff and the tax department were asked to refine ahead of follow-up sessions.

The report and presentation summarized how Act 73 changes Vermont's two-class system (homestead and nonhomestead) by adding the new class and moving to a statewide rate structure in which class-specific multipliers would be applied to a statewide base rate. "A new classification was introduced in act 73," Bellman said, and "rates are going to be uniform statewide," while the General Assembly could set multipliers annually.

Why it matters: the shift will change which property owners pay more, and will require extensive new data and municipal work. Bellman estimated the tax department will need to process "about a 173,000 homesteads" and "tens of thousands more" dwelling-use attestations, create or revise tax forms (a new dwelling-use attestation to replace the homestead declaration), and ensure towns can identify individual dwelling units by square footage and consistent identifiers.

Key implementation constraints include statutory dependencies and timing: new school district boundaries must be enacted by Jan. 1, 2027 for the mechanism to proceed, and multipliers will need to be set by July 1, 2028 to be effective for FY2029. Bellman called the statutory timeline "tight" and described the implementation as "doubly contingent" on those and other steps.

Committee members pressed for detail on several operational questions that remain unresolved in the report. Those include how to exclude long-term rentals from the new nonhomestead residential class, how to determine whether seasonal properties ("camps") are "fit for year-round application," whether municipalities can rely on external datasets (for example 9-1-1 records or landlord certificates) to locate dwelling units, and how land value should be apportioned when a parcel contains both residential and commercial uses. Bellman said some external datasets are imperfect and that towns will likely need to play a central role in verification.

Members also raised equity and enforcement concerns. Bellman noted Act 73 contains a default rule that would place units that appear fit for year-round habitation into the nonhomestead residential class unless an owner attests otherwise; he confirmed the default is deliberately adverse to encourage accurate reporting. The committee discussed penalties, appeals and whether to rely on the default rate as an incentive rather than expanding statutory fines.

The presentation included practical examples that highlight borderline and recurring cases: a single-family home converted to short-term rental; owner-occupied duplexes where one unit is vacant or periodically used by family; mixed commercial-residential buildings (a pottery studio with an apartment above); four-unit buildings with mixed short- and long-term rentals; and second homes with large outbuildings used commercially. For each example Bellman outlined how the dwelling-use attestation, square-footage apportionment and town records would determine classification and tax apportionment.

Next steps: the committee asked staff to draft decision points and a clear timetable. Chair Kornheiser asked Kirby Keaton to work with Julia Richter (JFO) and Bellman to produce a detailed timeline of decisions and statutory changes required over the next three years. The committee will revisit the decision tree and technical refinements in future meetings.

The committee did not take formal votes during this hearing. Members left several legislative questions unresolved (definitions of dwelling unit, land-value apportionment, precise penalty language) that staff and the tax department were asked to refine ahead of follow-up sessions.

Don't Miss a Word: See the Full Meeting!

Go beyond summaries. Unlock every video, transcript, and key insight with a Founder Membership.

✓

Get instant access to full meeting videos

✓

Search and clip any phrase from complete transcripts

✓

Receive AI-powered summaries & custom alerts

✓

Enjoy lifetime, unrestricted access to government data

30-day money-back guarantee