CHFA launches game-changing loan program to boost homeownership

August 28, 2024 | Consumer Protection Department, Departments and Agencies, Organizations, Executive, Connecticut

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

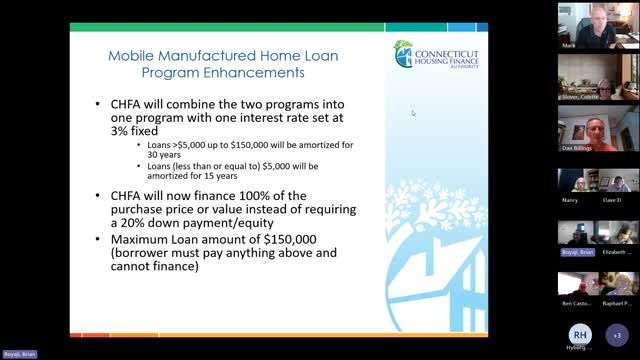

In a recent government meeting, officials discussed an innovative housing finance program proposed by the Connecticut Housing Finance Authority (CHFA), aimed at simplifying access to homeownership and refinancing options. The program, expected to launch in the fourth quarter of this year, combines existing refinance and purchase programs into a single offering with a fixed interest rate of 3%.

Currently, the purchase program operates at prevailing rates, around 6.375%, while the refinance program offers a low rate of 1% but requires a loan-to-value ratio of 80% or less. The new initiative will eliminate the need for a 20% down payment or equity requirement, allowing borrowers to finance 100% of either the purchase price or the appraised value of a property, up to a maximum loan amount of $150,000.

The CHFA has earmarked $5.75 million for this program, which aims to address the significant barriers faced by potential borrowers, particularly the challenge of meeting down payment requirements. Officials expressed optimism that this program will help more individuals qualify for loans, thereby facilitating home purchases and refinancing opportunities.

To promote the program, CHFA plans to utilize social media and provide downloadable flyers for realtors and community organizations. Suggestions were made during the meeting to further disseminate information through local planning commissions, enhancing outreach efforts to ensure that those in need are informed about the new financing options.

As discussions continue, stakeholders are encouraged to share ideas on effective communication strategies to maximize the program's impact in the community.

Currently, the purchase program operates at prevailing rates, around 6.375%, while the refinance program offers a low rate of 1% but requires a loan-to-value ratio of 80% or less. The new initiative will eliminate the need for a 20% down payment or equity requirement, allowing borrowers to finance 100% of either the purchase price or the appraised value of a property, up to a maximum loan amount of $150,000.

The CHFA has earmarked $5.75 million for this program, which aims to address the significant barriers faced by potential borrowers, particularly the challenge of meeting down payment requirements. Officials expressed optimism that this program will help more individuals qualify for loans, thereby facilitating home purchases and refinancing opportunities.

To promote the program, CHFA plans to utilize social media and provide downloadable flyers for realtors and community organizations. Suggestions were made during the meeting to further disseminate information through local planning commissions, enhancing outreach efforts to ensure that those in need are informed about the new financing options.

As discussions continue, stakeholders are encouraged to share ideas on effective communication strategies to maximize the program's impact in the community.

View the Full Meeting & All Its Details

This article offers just a summary. Unlock complete video, transcripts, and insights as a Founder Member.

✓

Watch full, unedited meeting videos

✓

Search every word spoken in unlimited transcripts

✓

AI summaries & real-time alerts (all government levels)

✓

Permanent access to expanding government content

30-day money-back guarantee