City faces $923000 deficit despite positive business activity

September 17, 2024 | Torrington, Northwest Hills County, Connecticut

This article was created by AI summarizing key points discussed. AI makes mistakes, so for full details and context, please refer to the video of the full meeting. Please report any errors so we can fix them. Report an error »

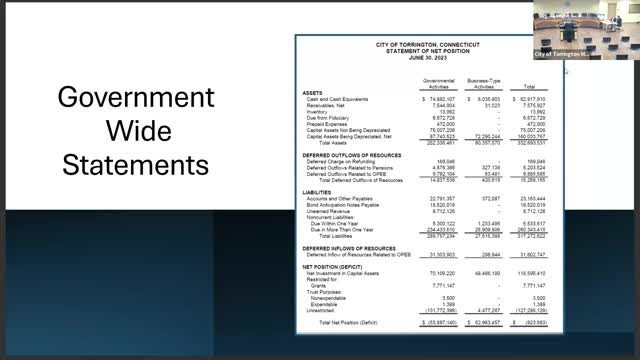

In a recent government meeting, officials reviewed the town's financial status as of June 30, 2023, revealing a complex fiscal landscape characterized by both deficits and positive net positions across various funds. The total net position for governmental activities showed a deficit of $53 million, while business-type activities reported a positive net position of approximately $52.9 million, resulting in an overall deficit of $923,000 for the year. This marks a significant decrease of $23.9 million in governmental activities, contrasted by a $41.2 million increase in business-type activities, leading to a net overall increase of $17.2 million from the previous fiscal year.

The meeting highlighted the town's fund financial statements, which are prepared on a modified accrual basis, excluding long-term assets and liabilities. The general fund's total balance stood at $18 million, down $418,000 from the previous year. Conversely, the bonded projects fund balance increased by $2.2 million to $10.3 million. Notably, the American Rescue Plan Act (ARPA) funds, totaling $6.8 million, remain unspent but must be obligated by December 31, 2024.

The Torrington High School renovation fund reported a significant decrease of $27.8 million, attributed to the timing of project expenditures. The non-major governmental fund balance increased by $4.9 million to $26.7 million. Internal service funds, including the self-insurance fund, showed a decrease in net position, while pension and OPEB trust funds reported increases, with the police and fire plan net position at $71.8 million and municipal employees at $42.9 million.

The meeting also addressed the city's pension liabilities, with the municipal employees plan funded at approximately 78% and the police and fire plan at about 63%. However, the net OPEB liability remains a concern, reported at $109.2 million and only 1.47% funded. Officials confirmed that the city is making annual contributions to address these liabilities.

Overall, the financial review underscored the importance of ongoing fiscal management and the need for strategic planning to navigate the town's financial challenges while ensuring compliance with funding obligations.

The meeting highlighted the town's fund financial statements, which are prepared on a modified accrual basis, excluding long-term assets and liabilities. The general fund's total balance stood at $18 million, down $418,000 from the previous year. Conversely, the bonded projects fund balance increased by $2.2 million to $10.3 million. Notably, the American Rescue Plan Act (ARPA) funds, totaling $6.8 million, remain unspent but must be obligated by December 31, 2024.

The Torrington High School renovation fund reported a significant decrease of $27.8 million, attributed to the timing of project expenditures. The non-major governmental fund balance increased by $4.9 million to $26.7 million. Internal service funds, including the self-insurance fund, showed a decrease in net position, while pension and OPEB trust funds reported increases, with the police and fire plan net position at $71.8 million and municipal employees at $42.9 million.

The meeting also addressed the city's pension liabilities, with the municipal employees plan funded at approximately 78% and the police and fire plan at about 63%. However, the net OPEB liability remains a concern, reported at $109.2 million and only 1.47% funded. Officials confirmed that the city is making annual contributions to address these liabilities.

Overall, the financial review underscored the importance of ongoing fiscal management and the need for strategic planning to navigate the town's financial challenges while ensuring compliance with funding obligations.

Don't Miss a Word: See the Full Meeting!

Go beyond summaries. Unlock every video, transcript, and key insight with a Founder Membership.

✓

Get instant access to full meeting videos

✓

Search and clip any phrase from complete transcripts

✓

Receive AI-powered summaries & custom alerts

✓

Enjoy lifetime, unrestricted access to government data

30-day money-back guarantee